Managing cross-border payments can drain your time and resources when running a European e-commerce business. Tracking expenses in euros, pounds, and zloty from multiple team members complicates accounting and raises the risk of overspending. A business debit card gives you immediate access to company funds without relying on credit and keeps business spending controlled across currencies. Discover how these cards simplify international purchases, enable real-time expense tracking, and offer practical tools for multi-currency operations.

Table of Contents

- Defining Business Debit Cards For Companies

- Types Of Business Debit Cards And Uses

- How Business Debit Cards Work For SMEs

- Multi-Currency And Cross-Border Capabilities

- Risks, Fees, And Comparisons To Alternatives

Key Takeaways

| Point | Details |

|---|---|

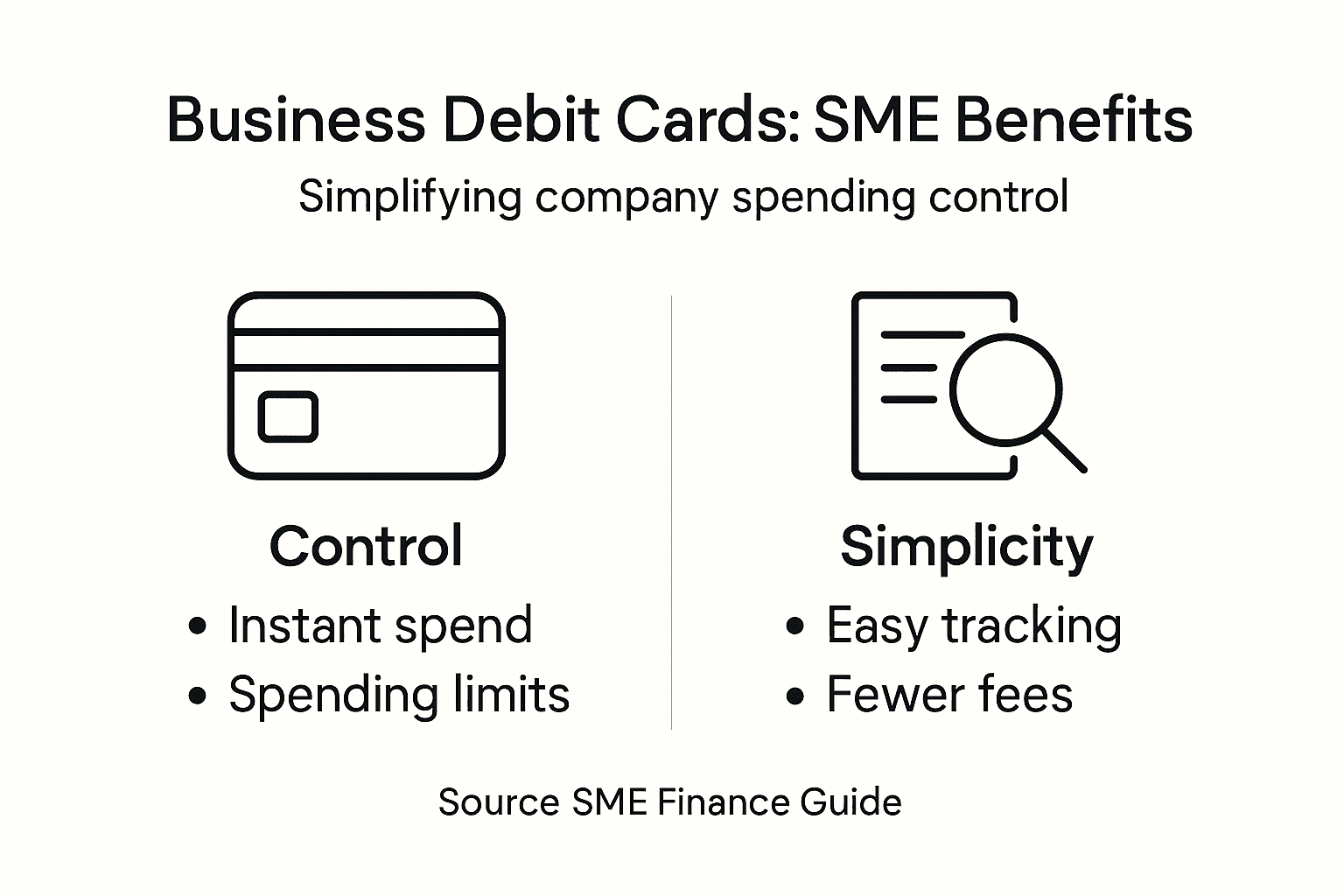

| Business Debit Cards Offer Immediate Access | They allow companies to spend directly from their bank accounts without incurring debt, promoting better cash flow management. |

| Founded on Spending Control | Business debit cards enforce spending limits, preventing unauthorized purchases and improving budget adherence. |

| Facilitates Real-Time Expense Tracking | Transactions are tracked immediately, providing businesses with clear visibility of cash flow and simplifying accounting processes. |

| Essential for Multi-Currency Operations | They are particularly beneficial for SMEs operating internationally, enabling seamless payments in local currencies without conversion hassles. |

Defining Business Debit Cards for Companies

A business debit card is a payment tool linked directly to your company's bank account. Unlike personal debit cards, it's designed exclusively for business expenses and gives you immediate access to funds without relying on credit.

Think of it as a controlled gateway to your business cash. When an employee swipes the card, the money comes straight from your business account. No credit extended, no monthly billing cycles to manage.

How Business Debit Cards Work

Core features include:

- Draws directly from business bank account funds

- Issued to multiple employees with customizable spending limits

- Tracks transactions in real-time for expense management

- Keeps business and personal spending completely separate

- Works online, in-store, and at ATMs for cash withdrawals

Your team receives a physical card or virtual card number to make purchases. Every transaction posts immediately, so you see exactly where company money goes. This direct account access eliminates the lag time of credit card settlements.

Key Differences From Credit Cards

Business debit cards operate fundamentally differently from business credit cards. A debit card pulls from existing funds, while credit cards extend short-term borrowing.

With a debit card, overspending becomes impossible—the transaction simply declines if insufficient funds exist. This built-in control matters enormously for budget management. You cannot accidentally rack up debt because you're spending what you actually have.

However, business debit cards do not build business credit history. If you're focused on establishing creditworthiness, a business credit card serves that purpose better. Most growing companies use both: debit cards for cash management and credit cards for credit building.

Why SMEs Benefit From Business Debit Cards

For small to medium-sized businesses, especially those managing multi-currency operations across Europe, business debit cards solve real problems.

Practical advantages:

- Real-time expense visibility across all employee purchases

- Reduced administrative burden compared to expense report processing

- Prevention of unauthorized or off-budget spending through spending limits

- Simplified employee reimbursement—no waiting for approval cycles

- Integration with accounting software for automated expense categorization

If your team handles international purchases, business debit cards work across multiple currencies when issued through platforms supporting euro, pound, and other major currencies.

For e-commerce operations specifically, having multiple team members with controlled access to funds eliminates bottlenecks. Your marketing manager can immediately purchase advertising credits. Your inventory coordinator can settle supplier invoices. Everyone operates within guardrails you set.

Business debit cards eliminate the approval delays that slow down growing companies while keeping spending under control through pre-set limits.

Pro tip: Set different spending limits for different employees based on their role and purchasing authority. A junior team member might have a €500 daily limit while your operations manager has €5,000, reducing approval friction without sacrificing oversight.

Types of Business Debit Cards and Uses

Business debit cards come in two main varieties: physical cards and virtual cards. Each serves different purposes depending on how your team conducts transactions.

Physical Business Debit Cards

Physical cards are traditional plastic cards your employees carry in their wallets. They work at point-of-sale terminals, ATMs, and anywhere accepting card payments.

These cards suit teams making regular in-person purchases. Your facility manager uses one to buy office supplies. Your operations coordinator settles invoices at supplier locations. The card provides immediate proof of payment and works offline.

Best for:

- In-store retail purchases

- ATM cash withdrawals for petty cash management

- Vendor payments requiring physical card presence

- International travel and local payments abroad

- Restaurant and hospitality expenses

Physical cards also create accountability. Employees sign receipts or enter PINs, leaving a clear transaction trail.

Here's how physical and virtual business debit cards serve different roles:

| Card Type | Best Suited For | Key Security Feature | Typical Use Case |

|---|---|---|---|

| Physical | In-person retail and travel | PIN or signature verification | Office supply or vendor payment |

| Virtual | Online and recurring payments | Unique number per transaction | SaaS subscriptions, marketing spend |

Virtual Business Debit Cards

Virtual cards exist only as digital numbers—no plastic involved. Your team uses the card number, expiration date, and CVV to make online purchases and phone payments.

Virtual cards focus on online payments and reduce fraud risk because each card number can be single-use or merchant-specific. You generate a temporary card number for one vendor, and that number becomes worthless after that transaction completes.

Best for:

- E-commerce purchases (software subscriptions, marketing platforms, inventory)

- Digital advertising spend across multiple channels

- SaaS tool subscriptions and recurring payments

- International online vendors

- Vendor onboarding when you need payment without sharing full account details

Virtual cards are perfect for your e-commerce operation. Your marketing team member gets a unique virtual card number for Google Ads. Your developer gets a different number for hosting services. Neither can use their assigned number anywhere else.

Hybrid Approach: Using Both Card Types

Most growing SMEs benefit from issuing both types. Physical cards handle the in-person needs while virtual cards manage online spending.

Your company might issue physical cards to three employees and virtual cards to eight others. The physical card users cover supplier visits and office expenses. The virtual card users handle online vendor management and digital tools.

Smart businesses issue multiple card types because physical and virtual cards solve different problems—physical for in-person control, virtual for online security.

Real-World Uses Across Your Team

Consider how different roles actually use business debit cards in practice.

Your procurement specialist uses a virtual card to purchase inventory from European suppliers, managing recurring weekly orders without repeated approval cycles.

Your operations manager carries a physical card for unexpected facility expenses, ensuring quick decisions during equipment emergencies.

Your marketing coordinator receives a new virtual card number weekly for testing different advertising platforms, preventing cross-platform spending and simplifying budget tracking.

Your warehouse staff accesses physical cards to settle last-minute shipping label fees when carriers demand immediate payment.

This combination keeps spending controlled while eliminating approval bottlenecks that slow down growing businesses.

Pro tip: Issue virtual cards for single-vendor purposes and rotate new numbers monthly, even for trusted suppliers, reducing the risk of unauthorized charges if card details leak into unsecured vendor systems.

How Business Debit Cards Work for SMEs

Business debit cards operate by drawing funds directly from your company's bank account. When someone swipes the card or enters the number online, money moves instantly from your business checking account to the vendor.

This immediate deduction differs fundamentally from credit cards, which create debt you settle later. Your team spends only what exists in the account—no credit extended, no monthly bills.

The Transaction Flow

Understanding the mechanics helps you implement cards effectively. Payments deduct directly from business account balances, ensuring real-time visibility into cash flow.

Here's how a typical transaction works:

- Card swipe or number entry - Employee makes a purchase using the physical card, virtual card number, or online payment

- Authorization check - The merchant's system contacts your bank to verify sufficient funds exist

- Funds deduction - If approved, money leaves your account immediately

- Transaction record - The charge appears instantly in your account dashboard

- Receipt and reconciliation - Documentation flows into your accounting system for tax records

This speed matters for growing European e-commerce businesses. Your inventory coordinator purchases stock from a German supplier at 9 AM. By 9:15 AM, the transaction settles and funds clear. No waiting for check clearing or wire processing delays.

Real-Time Expense Control

Business debit cards give you immediate visibility into company spending. Every transaction appears in your account the moment it completes, not days later.

Your accounting software integrates with the card system, automatically categorizing expenses. Marketing spend goes to the marketing budget. Office supplies go to operations. This automation eliminates manual expense reports and reconciliation headaches.

Key advantages:

- See exactly where money goes, instantly

- Prevent budget overruns through pre-set spending limits

- Eliminate expense report delays that slow approvals

- Reduce administrative work in expense categorization

- Maintain audit trails for tax compliance

Spending Limits and Controls

You assign specific limits to each employee card. Your junior coordinator might have a €500 daily limit while your procurement manager has €5,000.

When someone attempts a purchase exceeding their limit, the transaction declines. This built-in control prevents unauthorized spending without requiring approval for every transaction. Employees know their boundaries and can make decisions within them.

Limits work for both daily spending and transaction amounts. You could set a €2,000 daily maximum with a €500 limit per transaction. This prevents someone from accidentally (or intentionally) making one massive unauthorized purchase.

Business debit cards eliminate approval bottlenecks by pre-setting spending authority rather than requiring case-by-case authorization.

Multi-Currency Support for International Operations

For European SMEs managing cross-border transactions, business debit cards simplify international payments. Cards work globally for in-store and online payments, accepting local currencies and managing exchange rates automatically.

Your team pays Polish suppliers in zloty, German vendors in euros, and UK partners in pounds—all from one account dashboard. The card handles currency conversion behind the scenes, protecting you from surprise exchange rate markups.

Bookkeeping and Tax Benefits

Business debit cards create automatic records for tax compliance. Every transaction generates documentation showing who spent what, where, and when.

This eliminates the nightmare of employees losing receipts or mixing personal and business expenses. Your accountant can pull complete transaction reports directly from your card system for year-end tax filing.

Pro tip: Assign each employee a unique card or virtual card number so you can track individual spending patterns and identify which team members consistently exceed budgets or make off-category purchases.

Multi-Currency and Cross-Border Capabilities

European e-commerce businesses operate across borders constantly. You source inventory from Poland, sell to customers in France, and pay contractors in the United Kingdom. Managing multiple currencies through traditional banking creates friction, delays, and hidden costs.

Business debit cards solve this problem by enabling seamless multi-currency transactions without the typical banking hassles.

Spending in Local Currencies

When your team uses a business debit card abroad, the card automatically handles currency conversion. Your procurement specialist travels to a trade show in Amsterdam and pays vendors in euros directly from the card. No conversion required on your end, no separate accounts needed for each currency.

The card processes the transaction at competitive exchange rates, typically better than traditional bank transfers. You avoid the markup fees banks usually charge for currency conversion on wire transfers.

Key benefits:

- Pay suppliers in their local currency instantly

- Automatic exchange rate conversion without manual intervention

- Access to competitive rates rather than inflated bank markups

- No need to hold cash in multiple currencies

- Simplified vendor relationships through local currency payments

Managing Multiple IBAN Accounts

Growing European businesses benefit from multi-currency account structures that hold balances in different currencies simultaneously. Your company maintains a euro account for EU suppliers, a pound account for UK vendors, and a zloty account for Polish partners.

Business debit cards draw from whichever account matches the transaction currency. You pay a German supplier in euros—funds come from your euro balance. You settle a UK invoice in pounds—funds come from your pound balance.

This approach eliminates constant currency conversion and the associated costs. Money stays in its native currency until you actually need to spend it.

Real-Time Cross-Border Settlements

Traditional wire transfers take 2-5 business days. Your inventory team places an urgent order with a Czech supplier Monday afternoon. The wire doesn't clear until Thursday, potentially missing the shipment window.

Business debit cards settle instantly. Your team initiates the payment using the card, and the Czech supplier receives confirmation within minutes. No waiting for clearing cycles or international payment processing delays.

This speed matters enormously for e-commerce operations managing tight inventory windows and seasonal demand peaks.

Controlling International Spending

You set spending limits that apply globally. Your sales manager travels to trade shows across Europe with a card carrying a €3,000 weekly limit. No matter which country she's in, the limit stays consistent and prevents overspending.

You receive real-time alerts when transactions exceed thresholds, even across time zones. Your procurement team in Warsaw completes a large supplier payment at 2 AM your time—you see it instantly in your dashboard.

Control mechanisms:

- Per-transaction spending limits

- Daily or weekly spending caps

- Geographic restrictions (allow only European payments, for example)

- Real-time transaction alerts regardless of location

- Instant card freezing if suspicious activity occurs

Cross-border debit cards eliminate the 3-5 day settlement delays that disrupt international e-commerce operations while maintaining spending control across all currencies.

Simplified Accounting Across Borders

Managing expenses in multiple currencies traditionally requires constant manual reconciliation. Your accountant struggles to match invoices in euros to payments in pounds to account records in your home currency.

Business debit cards with integrated accounting software handle this automatically. Transaction data flows directly into your accounting system with the currency clearly marked. Your software automatically converts everything to your reporting currency using consistent exchange rates.

Tax reporting becomes simpler because you have complete transaction records with clear currency documentation for each purchase.

Pro tip: Use virtual cards generated in specific currencies for recurring vendor payments, such as a euro-denominated virtual card exclusively for your primary German supplier, which prevents accidental currency conversions and simplifies monthly reconciliation.

Risks, Fees, and Comparisons to Alternatives

Business debit cards offer simplicity and budget control, but they come with trade-offs. Understanding the limitations helps you make informed decisions about which payment tools your business actually needs.

Understanding Fee Structures

Business debit cards typically charge fewer fees than credit cards, but costs still exist. Common charges include ATM withdrawal fees, foreign transaction fees, and monthly maintenance fees depending on your provider.

ATM fees range from €1 to €3 per withdrawal at out-of-network machines. If your team frequently needs cash, these costs accumulate quickly. Foreign transaction fees typically run 1-3% of the transaction amount when paying international suppliers.

Typical fees include:

- Monthly account maintenance (€0-€15 depending on plan)

- ATM withdrawals at non-partner banks (€1-€3)

- Foreign transaction charges (1-3% per transaction)

- Card replacement fees (€5-€10 for physical cards)

- Inactivity fees if card unused for 6+ months

Compare these costs to your expected usage before committing. A business making 50 ATM withdrawals annually pays €50-€150 just in cash fees.

This summary highlights major risks and cost considerations with business debit cards:

| Risk or Fee Aspect | What to Watch | Business Impact |

|---|---|---|

| Fraud Protection | Limited dispute recourse | Potential financial loss on fraud |

| Foreign Transaction | 1-3% per transaction | Higher costs for global suppliers |

| ATM Cash Withdrawal | €1-€3 per withdrawal | Extra costs for frequent cash access |

| No Credit Building | No credit history gained | May limit borrowing capacity later |

Limited Fraud Protection and Recourse

Business debit cards offer reduced fraud protection compared to credit cards. If someone uses your card number fraudulently, recourse is more limited than with credit cards.

Credit cards shift liability to the card issuer. Debit cards often shift liability to you. If a vendor overcharges or doesn't deliver goods, disputing the charge takes longer and succeeds less frequently.

This matters more for high-value transactions. A €5 fraudulent charge is annoying but manageable. A €5,000 unauthorized supplier payment creates serious cash flow problems.

No Credit Building or Rewards

Business debit cards do not build your business credit score. Unlike credit cards, spending thousands monthly on debit cards leaves no credit history. This matters when you apply for business loans or lines of credit later.

Debit cards also offer no reward points, cashback, or travel benefits. Credit cards often provide 1-5% cash back on business purchases. Over a year, a business spending €100,000 annually loses €1,000-€5,000 in potential rewards.

Overspending Without Proper Monitoring

Debit cards prevent overspending beyond your account balance, but they don't prevent poor spending decisions. Your team can still spend frivolously within their limits.

Without real-time monitoring and alerts, you might not notice problematic spending patterns until month-end reconciliation. A team member consistently exceeds their limit for discretionary purchases, but you discover it weeks later.

Debit Cards vs. Credit Cards: Quick Comparison

| Feature | Debit Cards | Credit Cards |

|---|---|---|

| Fraud Protection | Limited | Comprehensive |

| Credit Building | No | Yes |

| Rewards/Cashback | None | 1-5% typical |

| Spending Control | Yes, enforced | Yes, optional |

| Approval Requirements | Minimal | Full underwriting |

| Fee Structure | Lower | Higher |

| Dispute Resolution | Slower | Faster |

The Right Tool for Each Purpose

Debit cards excel for expense control and immediate fund access. Credit cards excel for credit building and fraud protection. Growing European e-commerce businesses use both strategically.

Use debit cards for employee everyday spending. Use credit cards for recurring vendor payments where you need stronger fraud protection and want to build business credit history.

The best approach uses debit cards for operational expense control and credit cards for strategic purchases where protection and credit history matter.

Choosing Your Strategy

Start with debit cards for teams handling frequent small purchases. Your marketing team, operations staff, and supply chain coordinators benefit from immediate spending visibility and built-in limits.

Add credit cards for larger, less frequent transactions with trusted vendors. Your procurement manager uses a credit card for inventory purchases while your office manager uses a debit card for supplies.

Monitor both monthly to catch fee patterns. If ATM fees exceed €20 monthly, adjust your cash access method. If foreign transaction fees exceed 2% of international spending, negotiate better rates or find providers with lower charges.

Pro tip: Pair debit cards with a business credit card for specific vendor categories: use debit for vendor accounts over €50,000 annually and credit cards for vendors under that threshold, maximizing fraud protection where it matters most while controlling costs.

Unlock Seamless Business Spending with Multi-Currency Debit Cards

Managing business expenses across European borders can feel overwhelming. The article highlights the challenges SMEs face around real-time expense visibility, multi-currency support, and controlling employee spending through business debit cards. If you need to break free from approval delays and complex currency conversions while keeping spending limits tight, the right financial platform can make all the difference.

At Bankz, we specialize in empowering businesses with multi-currency digital business accounts and flexible physical and virtual VISA debit cards designed specifically for SMEs. Our solution streamlines international payments, spending controls, and expense management from a single easy-to-use dashboard. Say goodbye to hidden fees and slow settlements and hello to automated currency exchange and instant transaction tracking.

Take control of your business finances today by exploring how Bankz can simplify cross-border spending and give your team secure, tailored access to company funds. Start now and experience faster approvals, real-time monitoring, and unparalleled convenience for your growing business.

Frequently Asked Questions

What is a business debit card?

A business debit card is a payment tool linked directly to your company’s bank account, designed specifically for business expenses. It allows you and your employees to access funds in real-time without incurring debt, as transactions deduct directly from your business account.

How do business debit cards differ from credit cards?

Business debit cards pull funds directly from your existing business bank account, while credit cards allow short-term borrowing with scheduled repayments. Debit cards ensure you can only spend what you have, preventing overspending, whereas credit cards can build your business credit history.

What are the benefits of using a business debit card for SMEs?

Business debit cards offer real-time expense visibility, customizable spending limits for employees, simplified tracking and management of expenses, and eliminate the need for cumbersome expense reporting processes, making them ideal for small to medium-sized enterprises.

Can business debit cards be used internationally?

Yes, business debit cards can be used for international transactions, allowing businesses to make purchases in various currencies. They automatically handle currency conversion, making it easier to pay suppliers and vendors abroad without incurring additional bank fees.