Managing cross-border payments drains time and money for European SMEs. Traditional banking forces you to juggle multiple physical accounts, reconcile payments manually, and absorb steep transfer fees. Virtual IBANs solve this by cutting reconciliation time by up to 50% and reducing banking fees by 20-30%. This article explains what virtual IBANs are, how they work, and why they matter for your business in 2026.

Table of Contents

- Definition And Mechanism Of Virtual Ibans

- Benefits For Smes: Efficiency And Cost Reduction

- Benefits For Smes: Multi-Currency And Cross-Border Payments

- Regulatory And Security Considerations

- Common Misconceptions About Virtual Ibans

- Comparison Of Virtual Iban Providers

- Potential Limitations And Risks

- Real-World Applications And Case Studies

- Streamline Your Business Banking With Bankz

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Virtual IBANs are payment references | They link to one physical account but function as multiple sub-accounts for tracking. |

| They cut costs and speed reconciliation | Businesses see 50% faster reconciliation and 20-30% lower banking fees. |

| Multi-currency support is built in | Receive payments in multiple currencies without opening separate accounts. |

| PSD2 and GDPR compliance ensures security | Strong authentication and data privacy safeguards protect your transactions. |

| Provider features vary significantly | Check currency support and local payment scheme coverage before choosing. |

Definition and mechanism of virtual IBANs

A virtual IBAN is a unique payment identifier that routes funds to your physical bank account while acting as a separate reference point. Think of it as a labeled inbox within your main email account. Each virtual IBAN has its own number, but all payments land in the same underlying account.

This setup gives you the tracking power of multiple accounts without the administrative burden. When a client sends payment to a virtual IBAN, you instantly know which invoice or project it covers. No more guessing which payment matches which transaction.

Virtual IBANs streamline payment reconciliation by mapping each incoming transfer to a specific client, project, or invoice. This eliminates manual matching and reduces errors. Your bookkeeping system can automatically categorize transactions based on the virtual IBAN used.

They also support multi-currency and cross-border transactions without requiring separate physical accounts in each currency. This matters for SMEs handling payments from multiple European markets. You receive euros, pounds, and other currencies into one master account while maintaining clear separation through virtual identifiers.

Key features of virtual IBANs include:

- Act as multiple virtual sub-accounts under one physical account

- Provide unique IBAN numbers for segregating incoming payments

- Enable automatic payment-to-invoice matching

- Support SEPA, SWIFT, and local payment schemes

- Simplify multi-currency management for international SMEs

Benefits for SMEs: efficiency and cost reduction

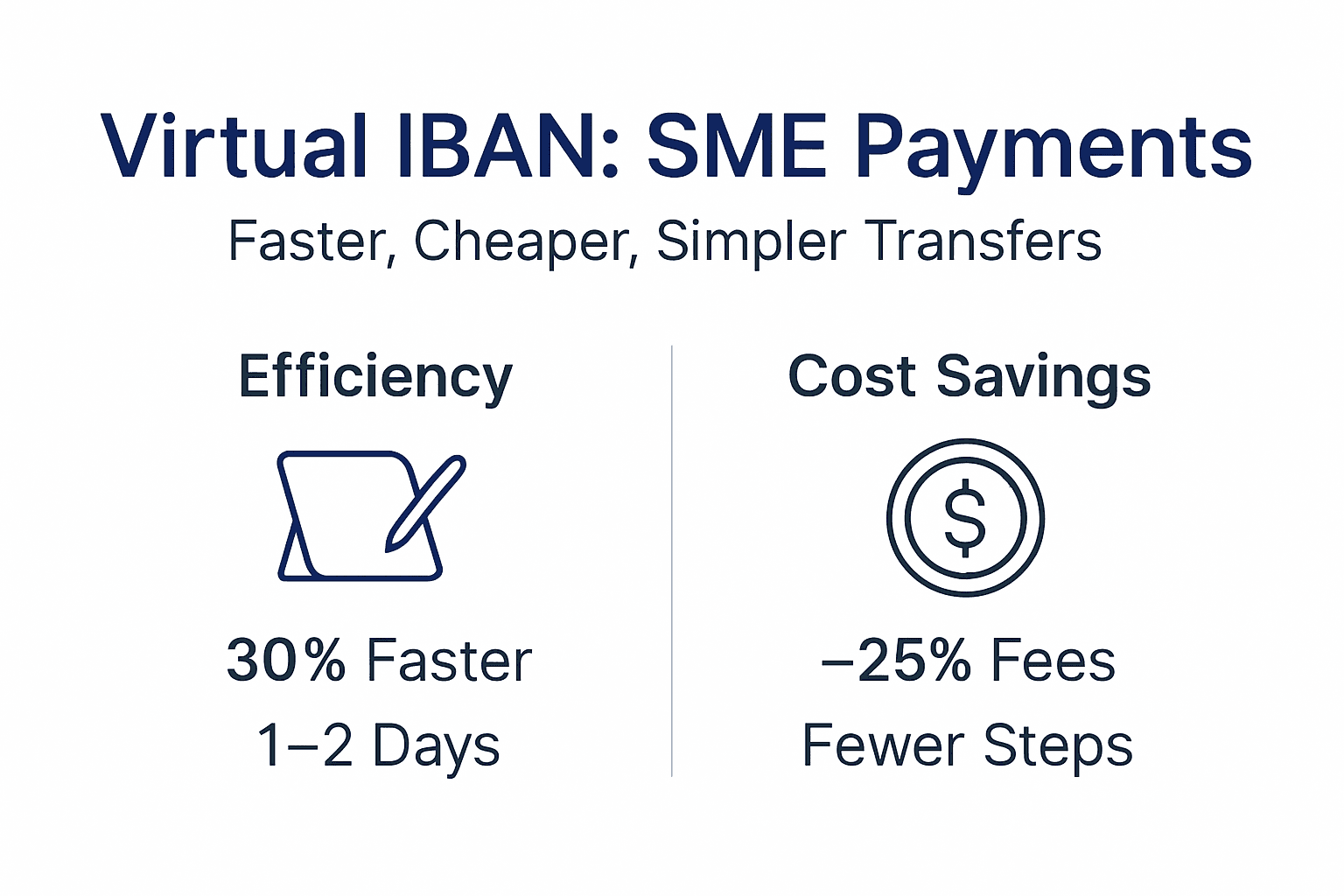

Virtual IBANs deliver measurable efficiency gains that translate directly to cost savings. Payment reconciliation time drops by up to 50% compared to traditional methods, freeing your finance team to focus on strategic work instead of data entry.

Banking fees for cross-border transfers decrease by 20-30% because virtual IBANs simplify payment routing. Traditional banks charge premium rates for international transfers that cross multiple intermediary banks. Virtual IBAN providers optimize routing to minimize these intermediary fees.

Invoice-level tracking enables clear, automated bookkeeping. When you assign a unique virtual IBAN to each client or project, your accounting software automatically categorizes incoming payments. This eliminates the monthly reconciliation headache where you match bank statements to invoices.

Reduced manual reconciliation accelerates cash flow visibility. You know in real time which clients have paid and which invoices remain outstanding. This matters for managing working capital and making informed business decisions.

Additional efficiency benefits:

- Lower administrative overhead for payment processing

- Fewer reconciliation errors and disputes

- Faster month-end financial close processes

- Simplified audit trails for tax compliance

- Better cash flow forecasting accuracy

Pro Tip: Assign a unique virtual IBAN to each major client or project. This gives you instant visibility into payment patterns and helps identify late-paying customers before they impact your cash flow.

Benefits for SMEs: multi-currency and cross-border payments

Virtual IBANs let you receive payments in multiple currencies without opening separate bank accounts in each country. This simplifies operations dramatically. Instead of maintaining accounts in Germany, France, and the Netherlands, you use one physical account with multiple virtual IBANs.

Payments clear faster internationally compared to traditional cross-border transfers. SEPA payments that normally take 2-3 days often settle within 24 hours when using optimized virtual IBAN routing. This improves your working capital position.

Centralized account monitoring improves financial oversight across regions. You view all currency balances and transactions from one dashboard instead of logging into multiple banking portals. This saves time and reduces the risk of overlooking important transactions.

Virtual IBANs reduce delays and fees for SEPA and other cross-border schemes by eliminating unnecessary intermediary banks. Traditional international transfers often pass through 2-3 correspondent banks, each taking a cut. Virtual IBANs route payments more directly.

They also simplify currency conversion and financial reporting for SMEs. You can hold multiple currencies in your account and convert them when exchange rates favor you, rather than accepting whatever rate your bank offers on the day payment arrives.

Multi-currency advantages:

- Accept payments in 15+ European currencies

- Faster settlement reduces payment float

- Single dashboard for all currency monitoring

- Flexible currency conversion timing

- Simplified multi-currency financial reporting

Regulatory and security considerations

Virtual IBANs operate within strict PSD2 compliance requirements that mandate strong customer authentication and secure payment processing. This means two-factor authentication, encrypted connections, and regular security audits protect your transactions.

GDPR mandates data privacy safeguards for handling client information. Virtual IBAN providers must protect customer data, limit access to authorized personnel, and notify you promptly of any security breaches. These rules apply across all EU member states.

Virtual IBANs do not have separate banking licenses and rely on a master physical account held by a licensed financial institution. This means your funds receive the same deposit protection as traditional bank accounts, typically up to €100,000 per depositor under EU schemes.

Security depends on provider systems, requiring trust and diligence on your part. Choose providers with ISO 27001 certification, regular penetration testing, and transparent security practices. Ask about their incident response procedures and uptime guarantees.

Understanding the regulatory context builds confidence in adopting virtual IBANs. These aren't unregulated fintech experiments. They operate under the same banking supervision as traditional accounts, just with a different technical implementation.

Regulatory protections:

- PSD2 strong customer authentication requirements

- GDPR data privacy and breach notification rules

- EU deposit insurance coverage on underlying accounts

- Regular regulatory audits of payment institutions

- Transparent fee structures mandated by law

Common misconceptions about virtual IBANs

Many SMEs mistakenly believe virtual IBANs are independent bank accounts. They're not. Virtual IBANs are payment references that route to a single master account. You can't withdraw cash directly from a virtual IBAN or maintain a separate balance in each one.

Virtual IBANs don't issue debit or credit cards separately. If you need payment cards, you get them from your underlying physical account, not from individual virtual IBANs. This confuses businesses expecting each virtual IBAN to function like a complete bank account.

Not all providers support all domestic European payment schemes. Some support SEPA and SWIFT but lack access to UK Faster Payments or Polish Elixir. This matters if you do significant business in specific countries. Verify scheme coverage before committing to a provider.

Virtual IBANs require a physical account as the base for operation and fund holding. You can't have virtual IBANs floating in space. There must be an underlying licensed bank or payment institution account where the actual money resides.

"Virtual IBANs are identifiers, not accounts. They tell the banking system where to route payments, but the funds themselves live in your master account. Understanding this distinction prevents costly mistakes."

Clearing these misconceptions prevents costly errors in provider selection:

- Virtual IBANs are references, not standalone accounts

- No separate card issuance per virtual IBAN

- Payment scheme support varies by provider

- Physical master account is always required

- Funds aggregate in the master account, not per virtual IBAN

Comparison of virtual IBAN providers

Choosing the right provider requires evaluating currency support, payment scheme access, API integration, and costs. Provider capabilities vary significantly, and the wrong choice can limit your operational flexibility.

| Feature | Provider A | Provider B |

|---|---|---|

| Currencies supported | 15+ including EUR, GBP, USD, CHF | 8 major European currencies |

| SEPA support | Full instant and standard | Standard SEPA only |

| UK Faster Payments | Yes | Limited |

| API integration | REST API with webhooks | Manual dashboard only |

| Monthly fee | €49 base + per-transaction | €29 base, higher per-transaction |

| Setup time | 24-48 hours | 3-5 business days |

Provider A supports 15+ currencies with full SEPA, Faster Payments access, and robust APIs for automation. This suits SMEs with high transaction volumes who need real-time data integration with their accounting systems. The higher base fee pays for itself through time savings.

Provider B supports fewer currencies and limited Faster Payments but offers a simpler dashboard and lower base fees. This works for smaller SMEs with straightforward needs who don't require API integration. Manual transaction downloads suffice for basic bookkeeping.

Choosing providers depends on your business priorities: processing speed, cost structure, and currency breadth. High-volume businesses benefit from API automation even with higher fees. Lower-volume businesses save money with simpler, cheaper options.

Some providers offer better automation with APIs, while others provide manual but low-cost setups. Match the provider's strengths to your operational needs. Don't pay for features you won't use, but don't skimp on capabilities you'll need as you grow.

Pro Tip: Verify local payment scheme support in your key markets before signing up. A provider without UK Faster Payments access will delay your British customer payments by 2-3 days compared to competitors.

Potential limitations and risks

Some providers lack coverage of all domestic European payment schemes such as Faster Payments, Elixir, or BACS. This creates payment delays in specific markets. If UK customers represent 30% of your revenue, a provider without Faster Payments support costs you speed and potentially customers.

Dependence on provider systems raises risk related to outages or policy changes. If your virtual IBAN provider experiences technical problems, your payment processing stops. You can't simply switch to another provider instantly because virtual IBANs are tied to specific routing infrastructure.

Virtual IBANs may restrict certain payment types or currencies depending on provider policies. Some don't support high-value transactions over €50,000. Others block payments from specific countries due to compliance concerns. Read the terms carefully.

Businesses should assess provider SLAs and compliance certifications before committing. Look for 99.9% uptime guarantees, 24/7 support availability, and clear incident response procedures. Check if they hold PSD2 payment institution licenses or operate as agents of licensed banks.

Understanding these limitations helps mitigate operational risks with virtual IBAN use:

- Incomplete payment scheme coverage delays some transactions

- Provider outages halt all payment processing temporarily

- Transaction limits may restrict high-value payments

- Geographic restrictions can block certain customer payments

- Provider policy changes can disrupt established workflows

Real-world applications and case studies

A Netherlands-based e-commerce SME reduced payment reconciliation time by 50% and cut banking fees by 25% after implementing virtual IBANs. They assigned unique identifiers to each sales channel, instantly knowing which payments came from their website versus marketplaces. This eliminated hours of manual matching each week.

A German consulting firm centralized multi-currency payments from clients in eight countries using virtual IBANs. They boosted cross-border sales by 40% because clients could pay in their local currency instead of dealing with conversion uncertainty. The firm's liquidity improved as payments cleared faster through optimized routing.

Streamlined invoice tracking enabled better financial forecasting and operations for both businesses. Real-time visibility into which clients had paid allowed them to make accurate cash flow projections and invest confidently in growth initiatives.

Virtual IBAN adoption demonstrated measurable ROI within three months for both companies. The Dutch e-commerce firm recovered the setup costs through reduced banking fees in the first quarter. The German consultancy's improved cash flow visibility prevented two instances of short-term overdraft borrowing.

Practical examples illustrate virtual IBAN impact beyond theory:

- E-commerce companies separate marketplace vs. direct sales payments

- Subscription businesses track recurring payments per customer automatically

- Freelance agencies assign virtual IBANs per client for project accounting

- Import/export firms manage multi-currency payments from global suppliers

- Professional services track payments by engagement or retainer

Streamline your business banking with Bankz

Managing cross-border payments doesn't have to drain your resources. Bankz offers virtual IBAN solutions integrated with multi-currency business accounts designed specifically for European SMEs like yours.

Our platform simplifies your cross-border payments and reduces banking fees through optimized routing and transparent pricing. You get seamless invoice tracking, faster payment clearing, and full PSD2 and GDPR compliance without the complexity of traditional banking.

Bankz lets you centralize all your European currency transactions efficiently from one dashboard. Whether you're receiving euros in France, pounds in the UK, or Swiss francs from clients in Zurich, everything flows into your master account with clear virtual IBAN identification.

We've built our international business bank accounts specifically for businesses that need reliable, cost-effective cross-border banking. Our setup process takes 24-48 hours, not weeks, and we support high-risk and non-conventional businesses other providers turn away.

Discover tailored international business bank account solutions that grow with your business. Start reducing your banking costs and improving your cash flow visibility today.

Frequently asked questions

What is a virtual IBAN?

A virtual IBAN is a unique payment identifier that routes incoming transfers to your physical bank account while providing a distinct reference for tracking purposes. It functions like a labeled sub-account but doesn't hold funds independently.

Do virtual IBANs operate as separate bank accounts?

No, virtual IBANs are payment references, not independent accounts. They cannot issue cards, maintain separate balances, or function autonomously. All funds flow into your underlying master account.

What advantages do virtual IBANs offer SMEs?

Virtual IBANs reduce payment reconciliation time by up to 50%, lower banking fees by 20-30%, and enable efficient multi-currency payment collection. They automate invoice matching and improve cash flow visibility significantly.

Are virtual IBANs secure and compliant?

Yes, virtual IBAN providers must comply with PSD2 strong authentication requirements and GDPR data privacy rules. The underlying master account typically receives EU deposit insurance coverage up to €100,000 per depositor.

How do I choose a virtual IBAN provider?

Evaluate currency support for your target markets, payment scheme access like SEPA and Faster Payments, API integration capabilities, and cost structure. Verify the provider holds proper PSD2 licensing and offers clear SLAs for uptime and support.