Many European SMEs assume a single international bank account handles all cross-border payment needs efficiently. This misconception costs businesses thousands in foreign exchange fees and delays cash flow by days or weeks. Opening multiple IBAN accounts transforms how you receive payments, converting slow international transfers into instant local transactions. You gain currency-specific accounts that eliminate conversion costs while accelerating settlement through SEPA Instant and Faster Payments. This guide reveals why multiple IBANs are essential for streamlined European business banking and how to implement them without operational complexity.

Table of Contents

- Why SMEs Need Multiple IBAN Accounts For Efficient Cross-Border Transactions

- Dedicated Versus Pooled And Virtual IBAN Accounts: Compliance And Operational Impact

- Navigating EU Regulations And High-Risk Sector Considerations With Multiple IBANs

- Best Practices For Managing Multiple IBAN Accounts To Boost Operational Efficiency

- Streamline Your Business Banking With Bankz Solutions

- Frequently Asked Questions About Opening Multiple IBAN Accounts

Key takeaways

| Point | Details |

|---|---|

| Multiple IBANs cut costs | Currency-specific accounts eliminate foreign exchange fees and speed up cross-border settlements through instant payment systems. |

| Dedicated IBANs reduce risk | Isolated accounts lower compliance burdens and audit complexity compared to pooled or virtual IBAN structures. |

| EU regulations tightened | New virtual IBAN rules require transparent master account linking and end-user identification to combat money laundering. |

| High-risk sectors prefer dedicated accounts | Crypto, iGaming, and regulated industries choose dedicated IBANs to avoid payment freezes and compliance complications. |

| Proper management boosts efficiency | Segmenting accounts by currency and maintaining clear audit trails optimizes financial operations and regulatory compliance. |

Why SMEs need multiple IBAN accounts for efficient cross-border transactions

Receiving payments in your customers' local currencies changes everything about international business banking. When you operate with multiple IBAN accounts, a German client paying in euros hits your EUR IBAN directly, settling within 10 seconds via SEPA Instant payment systems. A British customer sending pounds reaches your GBP IBAN through Faster Payments, processing instantly up to £1 million. Compare this to funneling all payments through a single account, where each transaction triggers currency conversion fees ranging from 2% to 5% and settlement delays stretching 2 to 5 business days.

The mathematics favor multiple accounts overwhelmingly. SMEs opening currency-specific IBAN accounts eliminate conversion costs entirely on local currency receipts. Your EUR IBAN receives euros, your GBP IBAN receives pounds, and your PLN IBAN receives zloty without touching foreign exchange markets. Settlement speed jumps from days to seconds because payments route through domestic clearing systems rather than correspondent banking networks.

Cash flow improvements compound these savings. Instant settlement means funds become available for immediate reinvestment, payroll, or supplier payments. You stop losing money to currency fluctuations during the 2 to 5 day settlement window typical of single-account international transfers. Payment tracking becomes transparent because each IBAN isolates specific currency flows, simplifying reconciliation and financial reporting.

Key benefits of multiple IBAN accounts:

- Local currency receipt eliminates foreign exchange conversion fees

- SEPA Instant and Faster Payments deliver funds within seconds, not days

- Transparent payment tracking improves reconciliation accuracy

- Reduced settlement risk from currency fluctuations during transfer windows

- Enhanced cash flow management through immediate fund availability

"Businesses using multiple IBANs report 40% faster payment processing and elimination of conversion fees on 70% of cross-border transactions, directly improving working capital efficiency."

The operational advantages of international business bank accounts extend beyond speed and cost. Multiple IBANs signal professionalism to international clients who prefer paying in their home currency. You reduce friction in the payment process, potentially shortening sales cycles and improving customer satisfaction. The infrastructure investment pays for itself within months for most SMEs handling regular cross-border transactions.

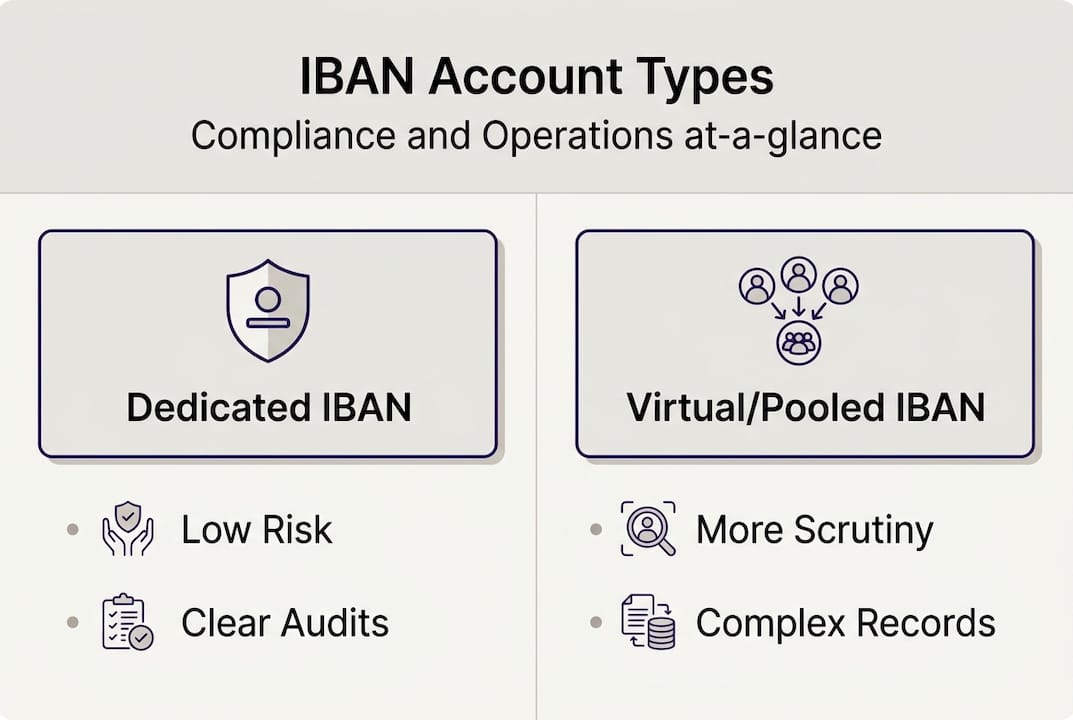

Dedicated versus pooled and virtual IBAN accounts: compliance and operational impact

Not all IBAN accounts function identically from a compliance and operational standpoint. Dedicated IBANs provide isolated accounts uniquely assigned to your business entity, operating independently within the banking system. Pooled and virtual IBANs share a master account among multiple users, with sub-account structures differentiating individual businesses. This architectural difference creates profound implications for audit readiness, compliance risk, and payment reliability.

Dedicated IBAN accounts offer isolated transaction histories that auditors can review without commingling concerns. When regulators or financial institutions investigate your account activity, they examine only your transactions. Pooled structures force reviewers to parse master account activity, potentially flagging unrelated transactions from other businesses sharing the pool. This complexity increases compliance review duration and raises the probability of payment holds or account freezes.

Compliance teams at banks apply heightened scrutiny to pooled and virtual IBAN arrangements because these structures historically attracted money laundering schemes. A single suspicious transaction from any business in the pool can trigger reviews affecting all participants. Your legitimate payment might freeze because another company sharing your master account triggered anti-money laundering alerts. Dedicated accounts eliminate this contagion risk entirely.

| Account Type | Compliance Risk | Audit Readiness | Payment Reliability | | --- | --- | --- | | Dedicated IBAN | Low (isolated reviews) | High (clear transaction history) | High (independent operations) | | Pooled IBAN | Medium (shared master account) | Medium (requires transaction parsing) | Medium (potential cross-contamination) | | Virtual IBAN | High (regulatory scrutiny) | Low (complex reporting requirements) | Low (frequent holds and reviews) |

Payment reliability differs markedly across account types. Dedicated IBANs rarely experience unexpected freezes because compliance reviews focus solely on your business activity. Virtual and pooled accounts face interruption risks from master account issues, technical problems with sub-account routing, or compliance flags from other users. For SMEs operating on tight cash flow margins, a 48-hour payment freeze can cascade into missed payroll or supplier defaults.

Pro Tip: If your business operates in regulated sectors like financial services, healthcare, or legal consulting, dedicated IBANs dramatically reduce operational disruption risk from compliance reviews and payment holds.

The cost differential between dedicated and virtual IBANs has narrowed significantly as fintech platforms democratize access to proper multiple business bank account management. Monthly fees for dedicated accounts now compete with virtual IBAN pricing while delivering superior compliance positioning. Factor in the hidden costs of payment delays, compliance investigation time, and potential account closures when comparing options.

Regulatory trends favor dedicated structures. Banking authorities increasingly require transparency in account ownership and transaction flows, making pooled arrangements more administratively burdensome. The influence of SEPA and IBAN standards in modern banking pushes toward clearer account attribution, which dedicated IBANs naturally provide.

Navigating EU regulations and high-risk sector considerations with multiple IBANs

European Union regulators tightened virtual IBAN oversight in 2025, implementing rules that took full effect in early 2026. The new framework requires transparent linking between virtual IBANs and master accounts with mandatory end-user identification reporting to combat anti-money laundering and counter-terrorist financing risks. Financial institutions must now trace every virtual IBAN transaction to a verified business entity and report beneficial ownership details to regulatory authorities quarterly.

These compliance requirements fundamentally altered the economics of virtual IBAN usage. Banks pass increased reporting costs to customers through higher monthly fees and transaction charges. More significantly, enhanced scrutiny means virtual IBAN transactions face longer processing times as compliance systems verify end-user identities and screen for suspicious patterns. What once offered a cost-effective alternative to dedicated accounts now carries comparable pricing with inferior operational performance.

High-risk industries like cryptocurrency exchanges, iGaming platforms, and forex brokers face amplified challenges with virtual IBANs. Regulators classify these sectors as elevated money laundering risks, triggering enhanced due diligence protocols. Over 30% of European SMEs cite compliance barriers as obstacles to adopting multiple IBAN strategies, with high-risk businesses reporting even higher friction rates approaching 50%.

Compliance barriers for high-risk sectors using virtual IBANs:

- Complex quarterly reporting requirements for beneficial ownership and transaction patterns

- Increased monthly costs from enhanced due diligence and monitoring obligations

- Extended payment processing times due to additional screening layers

- Higher probability of account freezes during routine compliance reviews

- Mandatory audit trail documentation exceeding standard banking requirements

Cryptocurrency and iGaming businesses increasingly choose dedicated IBANs despite higher upfront costs because operational reliability outweighs pricing considerations. A payment freeze lasting 72 hours can cost these businesses tens of thousands in lost revenue and customer trust. Dedicated accounts provide predictable operations with isolated compliance reviews that rarely interrupt payment flows.

"Regulatory changes affecting virtual IBANs have pushed over 30% of European SMEs toward dedicated account structures, with high-risk sectors leading this migration to ensure payment reliability and simplified compliance."

The regulatory landscape continues evolving toward greater transparency and accountability. Banking solutions for high-risk industries now emphasize dedicated IBAN structures that satisfy regulatory requirements while maintaining operational efficiency. Businesses in these sectors should budget for dedicated accounts as standard infrastructure rather than optional upgrades.

Compliance complexity extends beyond account type selection. Even with dedicated IBANs, high-risk businesses must maintain detailed transaction records, document business relationships, and provide regular updates to banking partners about operational changes. The impact of SEPA and IBAN regulations on web-based business banking means digital-first companies face the same scrutiny as traditional enterprises, eliminating any regulatory arbitrage from online operations.

Smart SMEs in high-risk sectors build compliance capabilities as core competencies rather than afterthoughts. Investing in proper documentation systems, staff training, and banking relationship management pays dividends in smoother operations and reduced regulatory friction. The cost of compliance pales compared to the business disruption from account closures or payment processing suspensions.

Best practices for managing multiple IBAN accounts to boost operational efficiency

Successfully operating multiple IBAN accounts requires systematic organization and disciplined financial management. Follow these proven steps to maximize benefits while minimizing administrative overhead:

-

Segment accounts by currency and country: Assign specific IBANs to distinct markets or currencies, creating clear operational boundaries that simplify tracking and reconciliation.

-

Maintain comprehensive records and audit trails: Document every transaction with supporting invoices, contracts, and correspondence to satisfy compliance requirements and streamline tax reporting.

-

Schedule regular compliance reviews: Conduct quarterly internal audits of account activity, flagging unusual patterns before they trigger bank investigations or regulatory inquiries.

-

Implement software tools for account management: Use treasury management systems or accounting platforms that aggregate multiple IBAN data into unified dashboards for real-time visibility.

-

Collaborate with banking partners to optimize fees: Negotiate volume-based pricing, request fee waivers for specific transaction types, and explore package deals that reduce per-account costs.

Proper management of multiple IBAN accounts directly improves operational efficiency by reducing reconciliation time, accelerating financial close processes, and providing clearer visibility into currency exposures. SMEs report 25% to 40% reductions in finance team hours spent on payment processing and account reconciliation after implementing structured multiple IBAN management practices.

| Best Practice | Primary Benefit | Implementation Difficulty |

|---|---|---|

| Currency segmentation | Simplified reconciliation and FX exposure tracking | Low (one-time setup) |

| Comprehensive record keeping | Audit readiness and tax compliance | Medium (ongoing discipline required) |

| Regular compliance reviews | Early issue detection and regulatory confidence | Medium (quarterly time investment) |

| Software integration | Real-time visibility and automated reporting | High (initial setup and training) |

| Banking partner collaboration | Reduced fees and improved service levels | Low (periodic negotiation) |

Pro Tip: Use dedicated IBANs for high-value or high-risk payment flows where reliability matters most, and consider virtual IBANs only for low-risk segmentation needs in jurisdictions where regulations permit simplified structures.

Staff training represents a critical but often overlooked component of multiple IBAN success. Finance teams need clear protocols for which account receives which payments, how to code transactions in accounting systems, and when to escalate unusual activity. Create simple decision trees and reference guides that eliminate guesswork from daily operations.

Optimizing financial management across multiple accounts requires balancing complexity against capability. Start with 2 to 3 IBANs covering your primary markets and currencies, then expand as operational proficiency grows. Rushing to open 8 or 10 accounts simultaneously overwhelms finance teams and creates reconciliation chaos.

Cash flow forecasting improves dramatically with proper multiple IBAN management because you gain granular visibility into currency-specific inflows and outflows. Build separate forecasts for each major currency, then consolidate to your reporting currency using realistic exchange rate assumptions. This approach reveals currency exposure risks that single-account structures obscure.

Technology selection matters enormously for multiple IBAN efficiency. Choose business bank account solutions offering API integrations with your accounting platform, automated transaction categorization, and multi-currency reporting capabilities. Manual data entry across multiple accounts wastes time and introduces errors that undermine the efficiency gains from better payment processing.

Streamline your business banking with Bankz solutions

Managing international payments across multiple currencies demands banking infrastructure built for cross-border complexity. Bankz delivers tailored international business bank account solutions with native multiple IBAN support, eliminating the friction SMEs face when scaling European operations. Our platform combines multi-currency accounts with business debit Visa cards that work seamlessly across your IBAN network.

You gain immediate access to EUR, GBP, and other currency IBANs through a single application process, with approval rates exceeding 95% even for high-risk industries. Reduce foreign exchange fees, accelerate payment settlement, and simplify compliance through our unified dashboard that aggregates all account activity. Business debit Visa cards and multi-currency accounts integrate with your IBANs for comprehensive expense management and payment flexibility.

Explore how enhanced business debit Visa card features combined with strategic multiple IBAN deployment can transform your international banking efficiency today.

Frequently asked questions about opening multiple IBAN accounts

What are the main advantages of opening multiple IBAN accounts?

Multiple IBAN accounts eliminate foreign exchange conversion fees on local currency receipts and accelerate payment settlement from days to seconds through SEPA Instant and Faster Payments systems. You gain transparent payment tracking, improved cash flow management, and professional credibility with international clients who prefer paying in their home currency.

How do EU virtual IBAN regulations affect my choice of account?

New 2026 EU regulations require virtual IBANs to link transparently to master accounts with quarterly end-user identification reporting, increasing costs and processing times. These compliance burdens make dedicated IBANs more attractive for most SMEs, offering simpler operations and lower regulatory friction.

Are dedicated IBAN accounts necessary for high-risk business sectors?

Yes, high-risk industries like crypto and iGaming benefit significantly from dedicated IBANs that provide isolated compliance reviews and reduce payment freeze risks. The operational reliability of dedicated accounts outweighs cost differences, preventing revenue loss from unexpected payment interruptions.

How can I manage multiple IBAN accounts without operational overload?

Implement currency segmentation, use treasury management software for unified dashboards, and maintain clear transaction documentation to streamline operations. Start with 2 to 3 IBANs covering primary markets, then expand gradually as your finance team builds proficiency with multi-account workflows.

Do multiple IBANs really reduce foreign exchange fees for SMEs?

Absolutely. Currency-specific IBANs receive local payments without conversion, eliminating 2% to 5% FX fees on those transactions. SMEs handling significant cross-border volumes report annual savings ranging from €5,000 to €50,000 depending on transaction volumes and currency mix.