Opening a business bank account for your European SMB sounds straightforward until you face rejection rates approaching 36%, hidden FX fees eroding margins, and compliance hurdles that delay operations for weeks. Cross-border transactions demand more than a basic account. You need multi-currency capabilities, transparent pricing, and streamlined onboarding that respects your time. This guide walks you through selecting the right banking partner, preparing bulletproof documentation, and setting up accounts optimized for international trade in 2026. You'll learn how to sidestep common pitfalls, cut currency conversion costs, and leverage digital tools that keep your global business running smoothly.

Table of Contents

- Understanding Your Business Needs And Banking Options

- Preparing Documentation And Meeting European Compliance Requirements

- Steps To Open Your International Business Bank Account Efficiently

- Avoiding Common Mistakes And Optimizing Your New Account

- Explore Bankz Solutions For Seamless International Business Banking

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Fintech vs traditional banks | Fintech providers deliver low fees and fast digital onboarding while traditional banks offer credit facilities but slower international transfers. |

| Documentation is critical | Incomplete or vague paperwork causes most rejections, so prepare detailed ownership structures and source of funds narratives upfront. |

| Multi-currency accounts save money | Holding funds in multiple currencies and using transparent FX rates can cut conversion costs by thousands annually. |

| Digital tools boost efficiency | Integrated expense management and real-time dashboards streamline cash flow and reduce administrative overhead. |

| Strategic provider selection matters | Choosing accounts with segregated funds, strong regulation, and international payment rails protects your business and accelerates growth. |

Understanding your business needs and banking options

Before you apply anywhere, identify what your business actually needs from a bank account. Do you process payments in multiple currencies weekly? Are you shipping products across borders or paying international suppliers? Maybe you need local IBANs in several countries to reduce transfer fees. Answering these questions narrows your search fast.

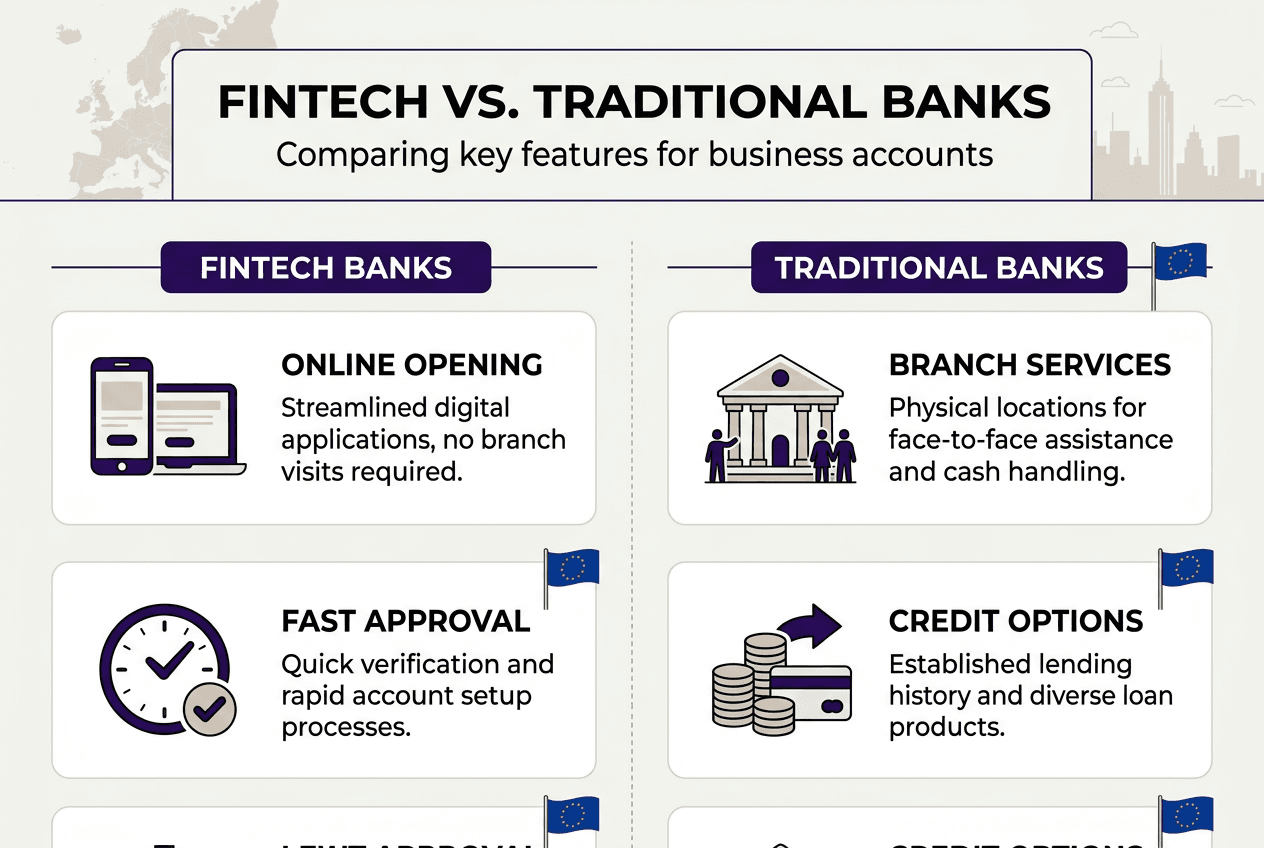

Fintech companies offer low-cost, easy-to-open business accounts regulated with segregated funds, making them ideal for SMBs focused on international trade. These digital-first providers prioritize speed, transparency, and global payment rails. You can open accounts remotely in days, access real-time dashboards, and manage multi-currency wallets without visiting a branch. They excel at SEPA, SWIFT, and local payment support.

Traditional banks still have advantages. They offer credit lines, overdrafts, and cash deposit services that fintech providers often skip. If your business relies on physical banking or needs lending facilities, a traditional bank might fit better. However, expect higher fees, slower international transfers, and more paperwork. Digital challenger banks and app-first providers compete directly with traditional lenders for SME customers, forcing improvements across the board.

Here's a quick comparison to guide your choice:

| Feature | Fintech Banks | Traditional Banks |

|---|---|---|

| Account Opening Speed | 1-3 days online | 1-4 weeks in person |

| Monthly Fees | €0-€15 | €15-€50+ |

| Multi-Currency Support | Native, low FX margins | Limited, high FX fees |

| International Transfers | Fast SEPA/SWIFT | Slower, costlier |

| Credit Facilities | Rare | Common |

| Cash Deposits | Not supported | Supported |

| Regulation | Licensed partners, segregated funds | Full banking license |

Pro Tip: Consider European fintech accounts for SMEs regulated with segregated partner banks. You get fintech agility plus the security of funds held separately from the provider's operating capital, combining the best of both worlds.

If your business handles frequent cross-border payments, prioritize providers with transparent FX rates and multi-currency wallets. If you need traditional services like loans or cash handling, a hybrid approach using both fintech and traditional accounts often works best. The key is matching banking features to your actual transaction patterns, not just picking the most popular name. Check fast business account approval in Europe to see how approval times vary by provider and business type.

Preparing documentation and meeting European compliance requirements

European banks operate under strict AML and KYC regulations that demand detailed documentation before approving your account. Up to 36% of EU business account applications are rejected due to incomplete documentation, so preparation matters more than you think. Rushing this step costs time and credibility.

You'll need these core documents for virtually every application:

- Company registration certificate or articles of incorporation proving legal entity status

- Proof of business address like a utility bill or lease agreement dated within the last three months

- Ownership structure chart showing all shareholders and beneficial owners with stakes over 25%

- Identity documents for all directors and significant shareholders, including passports and proof of address

- Recent financial statements or tax returns demonstrating business activity and revenue

- Business plan or narrative explaining your operations, revenue model, and target markets

- Source of funds documentation showing where initial capital originated

European banks require detailed ownership and source of funds explanations under tightening AML rules, especially if your business involves high-risk sectors or complex ownership chains. Vague answers trigger red flags. Banks want clear narratives about how your business makes money, who controls it, and where funds come from.

Common mistakes kill applications fast. Inconsistent information across documents raises suspicion. Failing to explain gaps in financial history or unusual transaction patterns invites rejection. Submitting outdated documents or missing signatures wastes everyone's time. Banks increasingly use automated screening tools that flag incomplete applications immediately, so double-check everything before submission.

Pro Tip: Prepare a compliance dossier answering potential bank questions before applying. Include a one-page business summary, ownership chart, source of funds statement, and projected transaction volumes. This proactive approach speeds approvals and signals professionalism.

If your business operates in sectors like crypto, gaming, or international trade with high-risk jurisdictions, expect extra scrutiny. Provide additional documentation showing compliance measures, transaction monitoring systems, and clear explanations of customer due diligence processes. Transparency beats evasion every time.

For practical guidance on assembling your documentation package, review the setup business bank account for UK and European businesses resource. It breaks down exactly what banks look for and how to present your information clearly. The effort you invest in preparation directly correlates with approval speed and account access.

Steps to open your international business bank account efficiently

Once your documentation is ready, follow these steps to open your account without unnecessary delays or complications.

-

Select the bank aligning with your business size and cross-border needs. Compare providers based on fees, supported currencies, international payment options, and approval rates for your business type. Wise Business offers local accounts in multiple currencies reducing conversion costs, while Revolut Business excels at fast SEPA transfers and expense management. Match features to your transaction patterns.

-

Gather and prepare documents addressing AML/KYC requirements. Use the checklist from the previous section. Ensure all documents are current, consistent, and clearly explain your business model and ownership structure. Missing or outdated paperwork is the top reason applications stall.

-

Submit application online or in person with a clear business narrative. Most fintech providers offer fully digital onboarding, while traditional banks may require branch visits. Include a concise explanation of your business operations, revenue sources, and expected transaction volumes. Clarity accelerates approval.

-

Set up multi-currency accounts for cost-efficient international payments. Once approved, activate currency wallets for every market you operate in. Holding funds in euros, pounds, dollars, and other currencies eliminates conversion fees on incoming payments and lets you pay suppliers in their local currency at better rates.

-

Integrate digital tools for streamlined cash flow and expense management. Connect accounting software, issue virtual cards for team expenses, and set spending limits by department. Automation reduces manual reconciliation and gives you real-time visibility into cash flow.

Here's how leading providers compare on key features:

| Provider | Monthly Fee | Currencies Supported | Approval Speed | FX Margin | | --- | --- | --- | --- | | Revolut Business | €0-€25 | 30+ | 1-2 days | 0.5-1% | | Wise Business | €0 | 50+ | 1-3 days | 0.35-0.65% | | Qonto | €9-€249 | EUR, USD, GBP | 1-3 days | 1-2% |

Cross-border payments with some traditional banks take more than one day and have costs over 3%, making fintech alternatives significantly more attractive for frequent international transactions. Speed and transparency matter when cash flow is tight.

Pro Tip: Opt for accounts with transparent, low FX fees and fast transfers to avoid cash flow bottlenecks. Check the international business bank benefits breakdown to see how multi-currency capabilities impact your bottom line.

After opening your account, test it with small transactions first. Verify that SEPA transfers arrive within hours, SWIFT payments clear as expected, and currency conversions reflect the rates you were quoted. This validation step prevents surprises when you start processing larger volumes. Use the business account setup checklist to ensure you've activated all relevant features and optimized settings for your business model.

Avoiding common mistakes and optimizing your new account

Even after successfully opening your account, poor management can erode the benefits you worked to secure. Many SMBs lose thousands annually to avoidable mistakes.

Common errors include:

- Submitting incomplete or inconsistent documentation during onboarding, triggering delays or rejection

- Choosing single-currency accounts when your business handles multiple currencies regularly

- Ignoring digital tools like expense management, automated reconciliation, or virtual cards

- Accepting high FX margins without comparing rates across providers

- Failing to monitor account fees and transaction costs as business volumes grow

High FX fees silently drain margins. Traditional banks often charge 2-3% on currency conversions, which compounds fast on large transactions. If you're converting €100,000 monthly, that's €2,000-€3,000 lost every month just on spreads. Fintech providers typically offer 0.35-1% margins, saving you significant capital over time.

CurrencyFair helped European businesses save over €50,000/year on FX fees by using peer-to-peer marketplace and low margins. Specialized FX providers leverage peer-to-peer matching to cut spreads even further than standard fintech accounts. For high-volume currency needs, they're worth investigating.

"A mid-sized European exporter reduced annual FX costs by €50,000 simply by switching from traditional bank conversions to a peer-to-peer FX platform. The savings went straight to operating margin without changing a single business process."

Pro Tip: Regularly review account fees and currency rates to adjust payment flows proactively. Set quarterly reminders to compare your current provider's rates against competitors. If you're processing high volumes, negotiate custom pricing or switch to better providers.

Optimize your account by using these strategies:

- Hold working capital in the currencies you'll spend it in, avoiding unnecessary conversions

- Schedule large FX conversions during favorable rate periods using limit orders or forward contracts

- Use virtual cards for online subscriptions and ad spend to track expenses by category automatically

- Set up automated reconciliation between your bank account and accounting software to eliminate manual data entry

- Review transaction reports monthly to identify patterns, spot anomalies, and forecast cash flow accurately

For comprehensive guidance on maximizing your account's value, explore streamline your business banking operations. The right tools and habits transform your account from a basic necessity into a strategic asset that actively improves cash flow and reduces costs.

Explore Bankz solutions for seamless international business banking

Now that you understand how to open and optimize a business bank account for cross-border success, consider how Bankz simplifies the entire process for European SMBs. Bankz multi-currency accounts and debit cards are built specifically for businesses managing international transactions, offering transparent FX rates, fast SEPA and SWIFT payments, and integrated expense management from a single dashboard.

You get multiple IBAN accounts, currency exchange at competitive rates, and business debit VISA cards that work globally without hidden fees. Bankz partners with licensed financial institutions to ensure your funds are segregated and secure while delivering the speed and flexibility fintech is known for. Whether you're paying suppliers in Asia, receiving payments from US clients, or managing payroll across Europe, Bankz handles the complexity so you can focus on growing your business. Discover how international business bank account solutions with Bankz can reduce your FX costs, accelerate approvals, and give you the financial infrastructure your global business deserves. Explore the benefits of international business bank accounts to see exactly how multi-currency capabilities and digital tools translate into real operational advantages.

Frequently asked questions

What documents are absolutely required to open a business bank account in Europe?

Mandatory documents typically include company registration certificate, proof of address, ownership details, and source of funds explanations. Banks also require detailed compliance info under AML regulations to verify legitimacy and beneficial ownership.

Can a fintech company's business account fully replace a traditional bank account for SMEs?

Fintech accounts offer low fees and easy multi-currency management but may lack credit and cash deposit services. Many SMEs use fintech for day-to-day banking while retaining traditional banks for lending and deposits.

How can I reduce currency conversion costs with my business bank account?

Choose accounts with transparent, low FX margins and access multi-currency wallets to hold funds in the currencies you need. Consider specialized FX service providers like CurrencyFair to save significantly on conversion fees for high-volume transactions.

What should I do if my business account application is rejected?

Review and enhance documentation, ensuring clear, consistent narratives about compliance and funds. Consult banking specialists or use fintech services with simpler onboarding to increase success rates and understand specific rejection reasons.