Many assume Euro business accounts are exclusive tools for large corporations. This belief misses a critical reality: over 75% of fintech Euro business account users are SMEs and startups. These specialized multi-currency banking solutions empower small to medium-sized businesses across Europe to manage cross-border transactions with unprecedented efficiency. For SMEs engaged in European trade, understanding what a Euro business account truly offers can transform operational workflows, reduce costs, and unlock competitive advantages previously reserved for enterprise-level players.

Table of Contents

- Understanding What A Euro Business Account Is

- Key Features And Regulatory Frameworks

- Multi-Currency Capabilities And Currency Exchange

- Benefits For SMEs Engaged In Cross-Border European Trade

- Common Misconceptions About Euro Business Accounts

- How To Choose And Open A Euro Business Account

- Conclusion: Maximizing SME Growth With Euro Business Accounts

- Streamline Your Business Banking With Bankz Solutions

- Frequently Asked Questions

Key Takeaways

| Point | Details |

|---|---|

| Multi-Currency Efficiency | Euro business accounts provide multiple IBANs enabling fast cross-border payments in euros and other currencies from one centralized platform. |

| Payment Infrastructure | SEPA and SWIFT integration streamline euro transfers and international payments while ensuring regulatory compliance. |

| SME-Focused Benefits | These accounts deliver up to 50% faster payment processing, reduced fees, and improved cash flow management tailored for growing businesses. |

| Accessibility Reality | Misconceptions about complexity are unfounded; modern fintech providers offer remote onboarding with approval rates exceeding 85%. |

| Selection Criteria | Choosing the right account requires evaluating fee structures, supported currencies, payment options, and compliance processes. |

Understanding What a Euro Business Account Is

A Euro business account is a specialized multi-currency business banking solution designed to facilitate seamless cross-border transactions within Europe. Unlike traditional single-currency accounts, these solutions provide multiple IBANs allowing you to receive and send payments in euros alongside other major currencies. This structure eliminates the need to open separate accounts in different countries.

The core purpose centers on simplifying international trade. When your business operates across European borders, managing payments in multiple currencies through disparate banking relationships creates administrative chaos. Euro business accounts consolidate this complexity into one dashboard where you control all cross-border financial activities.

Key functions include:

- Holding and transacting in multiple currencies simultaneously without conversion delays

- Processing SEPA transfers for fast, low-cost euro payments across participating countries

- Executing SWIFT transactions for international payments beyond the eurozone

- Managing multiple IBANs assigned to different countries or business units

- Automating currency exchange at competitive rates when needed

For SMEs engaged in European trade, centralized account management means reduced administrative burden. You avoid the paperwork, fees, and complexity of maintaining banking relationships in each country where you conduct business. This operational efficiency translates directly to time and cost savings.

Key Features and Regulatory Frameworks

Understanding the technical infrastructure behind Euro business accounts reveals why they deliver superior performance for cross-border operations. Three core systems form the foundation: SEPA, IBAN, and SWIFT.

SEPA (Single Euro Payments Area) revolutionized European banking by standardizing euro transfers across 36 countries. SEPA transfers typically settle within 1 business day with minimal fees, compared to traditional international transfers that often took 3 to 5 days. For SMEs, this speed improvement directly impacts cash flow and supplier relationships.

IBANs (International Bank Account Numbers) provide unique identifiers for accounts across countries. Modern Euro business accounts issue multiple IBANs, letting you receive payments as if you hold local accounts in Germany, France, Netherlands, and other European markets. Customers and partners send payments to local IBANs rather than foreign accounts, reducing their transfer costs and increasing payment success rates.

SWIFT integration handles payments outside SEPA territories or in non-euro currencies. While SEPA optimizes euro movements within participating countries, SWIFT connectivity ensures you can transact globally when business demands require it.

Regulatory compliance forms another critical layer. EU banking regulations mandate strict Anti-Money Laundering (AML) and Know Your Customer (KYC) procedures. Reputable Euro business account providers automate compliance checks, making onboarding smooth while maintaining security standards.

| Feature | Traditional European Business Account | Fintech Euro Business Account |

|---|---|---|

| Multi-IBAN Support | Limited, often requires separate applications per country | Multiple IBANs from single application |

| SEPA Processing Speed | 1-2 business days | Same day to 1 business day |

| Currency Options | Typically single or limited currencies | 10+ major currencies in one account |

| Remote Onboarding | Rare, usually requires branch visits | Standard offering with high approval rates |

| Fee Transparency | Complex, often hidden charges | Clear, competitive pricing structures |

| Compliance Automation | Manual documentation processes | Automated KYC/AML with digital verification |

Pro Tip: Before committing to any provider, verify their multi-IBAN capabilities cover the specific countries where you do business. Some platforms offer IBANs for major markets but lack coverage in smaller European economies where you might operate.

The integration of SEPA and IBAN explained systems creates the foundation for efficient European business banking. Understanding how SEPA and IBAN for business banking impacts daily operations helps you leverage these accounts fully. The influence of SEPA and IBAN operations extends beyond simple transfers to transform overall financial management.

Multi-Currency Capabilities and Currency Exchange

Managing multiple currencies represents one of the most powerful features Euro business accounts deliver to SMEs. Traditional banking forced businesses to open separate accounts for each currency, multiplying administrative tasks and fees. Modern solutions consolidate everything into a single platform.

Your account holds euros, British pounds, US dollars, and other major currencies simultaneously. When a customer in Sweden pays you in SEK or a supplier in Poland invoices in PLN, you receive and hold those currencies without immediate conversion. This flexibility lets you time currency exchanges strategically rather than accepting whatever rate applies when a payment arrives.

Currency conversion happens at competitive forex rates, typically much better than traditional bank markups. Banks often charge 3% to 5% above interbank rates plus fixed fees. Fintech Euro business account providers commonly offer rates within 0.5% to 1.5% of mid-market rates, delivering substantial savings on every conversion.

The streamlined process eliminates the need to transfer funds between multiple bank accounts before converting. You convert currencies within your dashboard with a few clicks. This simplicity reduces errors, saves time, and improves financial visibility.

Practical benefits extend beyond cost savings:

- Better cash flow control through strategic currency holding and conversion timing

- Simplified invoice reconciliation when receiving payments in the currency you billed

- Reduced foreign exchange risk by holding currencies you regularly pay out

- Faster vendor payments by holding their preferred currency ready for transfer

- Improved financial forecasting with clear visibility into multi-currency balances

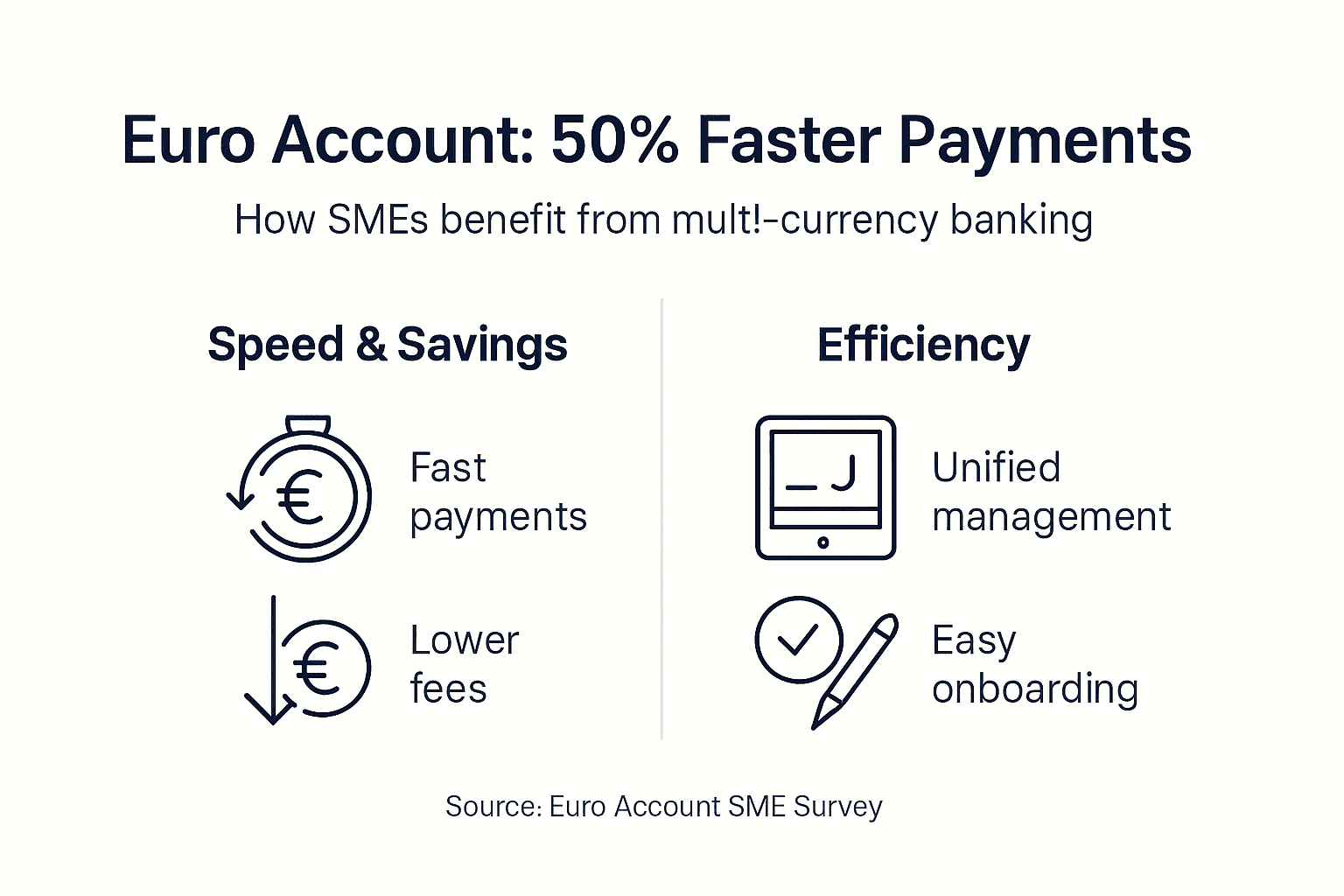

Businesses using multi-currency Euro business accounts report up to 50% faster payment processing and significant cash flow improvements. The speed advantage comes from eliminating conversion delays and maintaining ready balances in multiple currencies.

Pro Tip: Evaluate forex fee structures closely before selecting a provider. Some advertise zero fees but inflate exchange rates. Others charge small fixed fees with transparent near-market rates. Calculate total costs based on your actual transaction volumes and currency pairs to maximize savings.

The power of multi-currency management with SEPA becomes evident when you combine fast euro transfers with strategic currency holding. Understanding multi-currency and IBAN management helps you optimize international payment workflows.

Benefits for SMEs Engaged in Cross-Border European Trade

Translating features into tangible business outcomes reveals why Euro business accounts deliver competitive advantages for growing SMEs. The benefits extend far beyond simple cost reduction.

Payment processing speed increases dramatically. Where traditional international transfers consumed 3 to 5 business days, SEPA transfers through Euro business accounts settle in hours or one business day maximum. This 50% reduction in processing time means suppliers receive payments faster, improving relationships and potentially unlocking early payment discounts.

Transaction and currency exchange costs drop significantly. Eliminating multiple bank accounts removes monthly maintenance fees. Competitive forex rates save thousands annually for businesses with regular cross-border activity. Lower SEPA transfer fees compared to traditional SWIFT payments add further savings.

Unified management creates operational efficiency. Your finance team accesses all IBANs, currencies, and payment functions from one dashboard. This consolidation reduces training time, simplifies reconciliation, and minimizes errors from juggling multiple banking platforms.

Cash flow visibility improves through real-time balance tracking across all currencies and accounts. You see exactly what funds you hold where, enabling smarter financial decisions. Automation features streamline invoice reconciliation by matching incoming payments to outstanding invoices automatically.

Over 75% of fintech Euro business account users are SMEs and startups, proving these solutions deliver value precisely where growing businesses need it most.

"The majority of businesses leveraging modern Euro business accounts are small to medium enterprises and startups, not large corporations. This shift reflects how fintech has democratized access to sophisticated international banking infrastructure."

Top 5 SME benefits from Euro business accounts:

- Accelerated Payment Processing: Receive customer payments and pay suppliers 50% faster than traditional banking methods, directly improving working capital.

- Reduced Operating Costs: Save on monthly account fees, transaction charges, and currency conversion markups through consolidated, transparent pricing.

- Enhanced Professional Image: Issue invoices with local IBANs for each market, making it easier for customers to pay and positioning your business as established in their country.

- Simplified Compliance: Automated KYC and AML processes reduce administrative burden while maintaining regulatory adherence across multiple jurisdictions.

- Scalable Infrastructure: Add new currencies and IBANs as you expand into new markets without opening additional bank accounts or renegotiating banking relationships.

Integrating business debit cards for SMEs with your Euro business account extends these benefits to day-to-day spending. The combination of higher SME approvals and streamlined onboarding makes these solutions increasingly accessible. As cross-border business registrations grow across Europe, having the right banking infrastructure becomes essential for competitive success.

Common Misconceptions About Euro Business Accounts

Several persistent myths prevent SMEs from exploring Euro business account options. Correcting these misconceptions empowers better decision-making.

Myth: You need physical presence in an EU country to open an account. Reality: Many fintech providers allow fully remote onboarding, with approximately 90% applicant approval for remote setups. You submit documentation digitally, complete verification online, and access your account without ever visiting a branch.

Myth: Only large corporations benefit from these accounts. Reality: The user base proves otherwise. Over 75% of fintech Euro business account holders are SMEs and startups. The features, pricing, and support structures are specifically designed for smaller businesses managing cross-border trade.

Myth: Multi-country regulation makes these accounts too complex for small businesses. Reality: Compliance is automated and streamlined by providers. They handle regulatory requirements across jurisdictions, presenting you with simple onboarding checklists. You benefit from their expertise without needing to become a banking regulation expert.

Myth: Setup and maintenance costs outweigh the benefits for smaller transaction volumes. Reality: Many providers offer tiered pricing with low or no monthly fees for basic plans. Even businesses with modest cross-border activity save money through better forex rates and reduced transfer fees.

Myth: These accounts lack the security and reliability of traditional banks. Reality: Reputable fintech providers partner with licensed financial institutions and maintain the same deposit protection schemes as traditional banks. They often exceed traditional banks in security features through advanced digital authentication.

Key contrasts between myths and facts:

- Myth: Complex application processes requiring extensive documentation. Fact: Streamlined digital onboarding typically completed in 24 to 48 hours.

- Myth: Limited customer support compared to traditional banks. Fact: Many fintech providers offer superior support through chat, email, and phone with faster response times.

- Myth: Restricted functionality compared to full-service banks. Fact: Euro business accounts often provide more advanced features for cross-border payments than traditional banks.

- Myth: High rejection rates for SMEs without established credit history. Fact: Approval rates exceed 85% for compliant businesses, with more flexible evaluation criteria than traditional banks.

Understanding remote onboarding for Euro business accounts removes barriers many SMEs assume are insurmountable. Modern providers have eliminated most friction points that made international business banking difficult for smaller companies.

How to Choose and Open a Euro Business Account

Selecting the right Euro business account requires systematic evaluation of your needs against provider capabilities. Follow this process to make an informed choice.

Evaluate these key criteria:

- Fee Structure: Compare monthly maintenance fees, transaction charges, currency conversion markups, and IBAN issuance costs. Calculate total costs based on your projected transaction volumes.

- Currency Support: Verify the provider supports all currencies you need now and likely will need as you grow.

- Payment Options: Confirm SEPA, SWIFT, and any local payment scheme access required for your markets.

- Integration Capabilities: Check if the account connects with your accounting software, e-commerce platforms, or other business tools.

- Compliance Requirements: Understand what documentation and verification they require. Some providers have more stringent requirements than others.

- Customer Support: Evaluate support availability, response times, and expertise in serving businesses similar to yours.

Prepare required compliance documentation before applying. Standard requirements include:

- Business registration documents (incorporation certificate, articles of association)

- Proof of business address

- Identification documents for beneficial owners and authorized signatories

- Business activity description and projected transaction volumes

- Source of funds documentation

Remote onboarding possibilities and approval rates are now typically above 85% for compliant SMEs, making the process much faster than traditional banking.

Stepwise process for account selection and opening:

- Assess Your Needs: List the currencies, countries, and payment types your business requires now and in the next 12 months.

- Research Providers: Identify 3 to 5 Euro business account providers serving your industry and geography. Review their features, pricing, and customer feedback.

- Request Detailed Information: Contact shortlisted providers for complete fee schedules and feature comparisons. Ask specific questions about your use cases.

- Compare Total Costs: Calculate projected annual costs including all fees and estimated currency conversion charges based on your transaction patterns.

- Initiate Application: Submit your application with the strongest candidate. Prepare all documentation beforehand to speed approval.

- Complete Verification: Respond promptly to any verification requests. Most providers complete KYC checks within 24 to 72 hours.

- Configure Account Features: Once approved, set up your IBANs, currency accounts, user permissions, and integrations according to your operational needs.

- Test Functionality: Conduct small test transactions to verify SEPA, SWIFT, and currency conversion work as expected before processing larger payments.

Leveraging remote onboarding means you can establish international banking infrastructure without travel or time zone complications. The entire process from application to active account typically completes in 3 to 7 business days.

Understanding how to open a Euro business account with remote capabilities removes geographic barriers. You gain access to European banking infrastructure regardless of where your business is physically located.

Conclusion: Maximizing SME Growth with Euro Business Accounts

Euro business accounts have transformed from corporate-exclusive tools to essential infrastructure for SMEs engaged in European trade. The combination of faster payments, reduced costs, and multi-currency management delivers competitive advantages that directly impact growth trajectories.

Operational efficiency improves when you consolidate cross-border banking into one platform. Your finance team spends less time managing multiple banking relationships and more time on strategic activities. Cash flow visibility increases through real-time tracking across currencies and accounts.

The evidence is clear: businesses leveraging these solutions process payments 50% faster, reduce transaction costs significantly, and scale more easily into new European markets. As cross-border commerce continues expanding, the SMEs with proper banking infrastructure will outpace competitors still struggling with traditional banking limitations.

Consider exploring modern fintech providers like Bankz.eu that specialize in delivering these capabilities to growing businesses. The right Euro business account transforms international banking from an operational headache into a strategic advantage.

Streamline Your Business Banking with Bankz Solutions

Ready to implement everything you've learned about Euro business accounts? Bankz delivers exactly what growing SMEs need for efficient cross-border European trade.

Our platform provides multi-currency accounts and debit cards designed specifically for businesses like yours. You get multiple IBANs across European markets, enabling fast SEPA transfers that settle in hours rather than days. SWIFT connectivity ensures you can transact globally when needed.

Remote onboarding takes minutes, not weeks. Our streamlined verification process achieves high approval rates for SMEs, even those in specialized industries. Once active, you manage everything from a unified dashboard: track balances across currencies, execute transfers, reconcile invoices, and control spending through integrated business Visa debit cards.

The benefits of international business bank accounts and multi-currency accounts become immediately tangible when you have the right partner. Bankz combines competitive pricing with powerful features, giving you international business bank account solutions with Bankz that scale as your European operations grow.

Frequently Asked Questions

What is a Euro business account and who can open one?

A Euro business account is a multi-currency business banking solution enabling seamless cross-border transactions within Europe through multiple IBANs and integrated SEPA/SWIFT capabilities. SMEs, startups, online businesses, and even high-risk industries can open these accounts, with modern fintech providers approving over 85% of compliant applications regardless of business size.

How does a Euro business account handle multiple currencies?

These accounts let you hold, receive, and send payments in euros plus other major currencies from a single platform. You convert between currencies at competitive rates within your dashboard, timing exchanges strategically rather than accepting automatic conversion at unfavorable rates. This flexibility reduces costs and improves cash flow management.

Is a physical branch visit necessary to open a Euro business account?

No, modern Euro business account providers offer fully remote onboarding with approximately 90% approval rates for digital applications. You submit documentation online, complete verification digitally, and access your account without visiting any physical location. The entire process typically completes in 3 to 7 business days.

What are the main fees associated with Euro business accounts?

Fee structures vary by provider but typically include monthly maintenance fees (often waived for basic plans), transaction fees for transfers, currency conversion markups, and occasionally IBAN issuance charges. Reputable fintech providers offer transparent pricing with competitive rates, often significantly lower than traditional banks. Always calculate total projected costs based on your actual transaction volumes.

How can SMEs benefit operationally from these accounts?

SMEs gain faster payment processing (up to 50% reduction in settlement time), reduced transaction and currency exchange costs, unified management of multiple currencies and IBANs, improved cash flow visibility, and simplified compliance through automated processes. These operational improvements free resources for growth activities rather than administrative banking tasks.

Can Euro business accounts integrate with existing business software?

Most modern Euro business account providers offer integration capabilities with popular accounting software, e-commerce platforms, and payment processors. This connectivity automates reconciliation, synchronizes financial data, and reduces manual data entry. Check integration options with your specific software stack when evaluating providers.

Recommended

- Fast Business Account Approval: Unlocking Cross-Border Payments

- Business Account Verification: 40% Higher SME Approvals

- Setup Business Bank Account for UK and European Businesses

- Business Plan Expert-Comptable | Banques & Administrations

- Automatisierte Angebote Und Rechnungen | Univents Finanzdokumente