Managing business finances across borders and multiple currencies can feel like juggling flaming torches, especially when multiple team members need access to banking operations. Many small to medium business owners believe a multi-user business account is simply a standard account where several people share login credentials. That's a dangerous misconception. True multi-user business accounts provide sophisticated role-based access, security controls, and operational transparency that transform how European SMBs handle cross-border transactions. This guide clarifies what these accounts actually are, how they work, and why they're essential for businesses operating in today's interconnected European marketplace.

Table of Contents

- Key takeaways

- What is a multi-user business account?

- How multi-user business accounts differ from traditional business accounts

- Benefits of multi-user business accounts for European SMBs

- How to set up and manage a multi-user business account effectively

- Streamline your business banking operations with Bankz

- Frequently asked questions about multi-user business accounts

Key Takeaways

| Point | Details |

|---|---|

| Role Based Access | Multi user accounts assign permissions by job function to prevent permission sprawl and improve security. |

| Tenant Isolation | Tenant isolation prevents data leaks between entities or divisions sharing the same banking infrastructure. |

| Audit Logs | Audit logs provide a tamper resistant record of who did what and when in the account. |

| Cross Border Payments | They support cross border and multi currency transactions essential for European SMBs expanding internationally. |

What is a multi-user business account?

A multi-user business account is a business banking solution that allows multiple authorized individuals to access and manage company finances simultaneously, each with distinct permissions tailored to their specific role. Unlike traditional accounts where one or two people hold all access rights, these accounts implement sophisticated security frameworks designed for modern business complexity.

The foundation of these accounts rests on role-based access control (RBAC), which assigns permissions based on job functions rather than individual identities. This approach prevents what security experts call "role explosion," where organizations create too many overlapping permission sets that become impossible to manage effectively. Implementing RBAC with tenant isolation prevents information leaks between different business entities or branches operating within the same banking infrastructure.

Tenant isolation acts as a digital wall between different organizational units. If you're managing multiple business bank accounts or operating separate divisions, this feature ensures financial data from one entity never accidentally appears in another's view. It's particularly crucial for holding companies or businesses with multiple subsidiaries.

Audit logs provide the transparency layer that makes multi-user environments trustworthy. These logs automatically track every action taken within the account, recording who initiated transactions, approved payments, or modified account settings, along with precise timestamps. For European SMBs handling cross-currency payments and working with team members across borders, this creates an unalterable record that satisfies both internal governance needs and external compliance requirements.

Pro Tip: When setting up your multi-user account structure, start with broad role categories like "payment initiator," "approver," and "viewer" before creating specialized roles. This prevents permission sprawl while maintaining security.

The practical value becomes clear when you consider daily operations. Your accountant can view transaction history and generate reports without ability to initiate payments. Your operations manager can process supplier payments but cannot modify user permissions. Your CFO maintains oversight across all activities without needing to personally execute routine transactions. This division of responsibilities creates natural checks and balances while accelerating workflow.

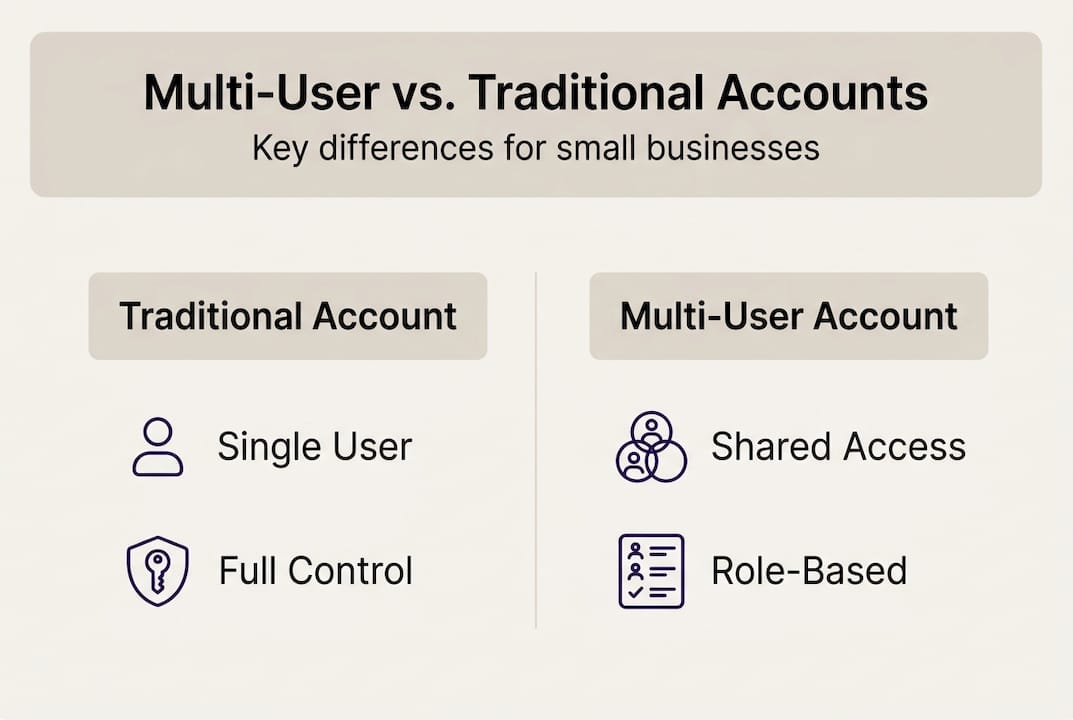

How multi-user business accounts differ from traditional business accounts

Traditional business bank accounts typically authorize one or two signatories who hold complete control over all banking functions. Everyone else either has no access or must physically visit the bank with authorized signers to conduct business. This model made sense when businesses operated locally with small teams, but it creates significant friction for modern SMBs.

Multi-user business accounts flip this paradigm entirely. They allow organizations to grant access to dozens of users simultaneously, each operating within carefully defined boundaries. Your marketing team can access the company card for ad spend without seeing payroll transactions. Your accounts payable clerk can process vendor payments without ability to transfer funds to external personal accounts. This granular control transforms financial management from a bottleneck into a streamlined operation.

The security architecture differs fundamentally. Traditional accounts rely on password protection and perhaps two-factor authentication for the limited authorized users. Multi-user accounts layer on RBAC, tenant isolation, and comprehensive audit trails that create multiple security checkpoints. If a user's credentials are compromised, the damage is contained to their specific permission set rather than exposing the entire account.

Here's how they compare across critical dimensions:

| Feature | Traditional Business Account | Multi-User Business Account |

|---|---|---|

| Authorized Users | 1-2 signatories with full access | Unlimited users with role-specific permissions |

| Access Control | All-or-nothing permissions | Granular RBAC with customizable roles |

| Security Monitoring | Basic transaction alerts | Comprehensive audit logs tracking all user actions |

| Multi-Currency Support | Limited, often requires separate accounts | Integrated multi-currency management in single account |

| Cross-Border Payments | Manual processes, higher fees | Streamlined SEPA, SWIFT, and local payment options |

| Workflow Efficiency | Sequential approval processes | Parallel task execution by multiple users |

| Compliance Documentation | Manual record keeping | Automated audit trails and reporting |

The operational impact is substantial. With traditional accounts, the business owner or finance director becomes a bottleneck for every payment approval, account inquiry, or transaction verification. Best practices for managing business accounts emphasize delegation, which simply isn't possible without proper multi-user infrastructure.

Multi-user accounts also excel at supporting international operations. Traditional accounts often struggle with currency conversion, cross-border payment rails, and compliance with varying European banking regulations. Modern multi-user platforms integrate these capabilities natively, allowing your London office to pay suppliers in pounds while your Berlin team handles euro transactions, all within the same account structure and oversight framework.

Benefits of multi-user business accounts for European SMBs

European small and medium businesses face unique operational challenges that multi-user business accounts address directly. The ability to delegate financial responsibilities while maintaining oversight transforms how SMBs scale across borders and manage growth.

Delegated access with full visibility stands as the primary advantage. You can grant your external accountant read-only access to generate reports without exposing sensitive operational data. Your warehouse manager can approve supplier payments up to defined limits without requiring your personal sign-off for every transaction. Each department operates autonomously within guardrails you establish, while you maintain complete transparency through comprehensive audit logs and activity monitoring.

Multi-currency functionality eliminates one of the biggest pain points for European businesses operating across borders. Rather than maintaining separate accounts in different currencies or paying excessive foreign exchange fees, international multi-currency accounts let you collect, hold, and disburse funds in dozens of currencies. Your French clients can pay in euros, your British suppliers receive pounds, and your Polish contractors get zloty, all managed from a single dashboard without conversion delays or unnecessary fees.

Cross-border payment facilitation becomes straightforward rather than complex. Multi-user accounts designed for European markets integrate seamlessly with SEPA for euro-zone transfers, provide IBAN accounts for receiving international payments, and support SWIFT for global transactions. This integrated international banking approach means your accounts payable team can process payments to suppliers across Europe as easily as domestic transfers.

Cash flow management improves dramatically when multiple stakeholders can monitor financial activity in real time. Your sales team sees incoming payments immediately, allowing them to release orders without waiting for finance department confirmation. Your procurement team checks available balances before committing to large purchases. Your CFO reviews spending patterns across departments without manually requesting reports from various team members.

Pro Tip: Set up automated notifications for transactions above specific thresholds to different user groups. This creates early warning systems for unusual activity without requiring constant manual monitoring.

Compliance and internal reporting become simpler when your banking infrastructure automatically documents every action. European regulations around financial record keeping, anti-money laundering, and transaction reporting are satisfied through the built-in audit trail. When tax time arrives or auditors request documentation, you can generate comprehensive reports showing who authorized what payments, when approvals occurred, and how funds moved through the organization.

How to set up and manage a multi-user business account effectively

Setting up a multi-user business account requires strategic planning to balance security, usability, and operational efficiency. Follow these steps to implement a system that scales with your business:

-

Map your organizational structure and identify distinct financial roles within your business. Document who needs to initiate payments, who should approve them, who requires read-only access for reporting, and who manages user permissions themselves.

-

Choose a banking provider that explicitly supports tenant isolation and maintains comprehensive audit logs for security and compliance. Verify they offer the specific currency accounts and cross-border payment methods your business requires.

-

Design your permission structure using RBAC principles, creating broad role categories before specialized ones. Start with essential roles like payment initiator, payment approver, report viewer, and account administrator to avoid role explosion.

-

Configure multi-currency capabilities by opening accounts in each currency your business regularly transacts in. Ensure your provider supports SEPA transfers, IBAN receiving accounts, and any specific payment rails important to your operations.

-

Implement your user access plan by assigning team members to appropriate roles, providing training on their specific permissions, and documenting the approval workflows for different transaction types.

-

Establish monitoring procedures by setting up automated alerts for transactions above certain thresholds, scheduling regular audit log reviews, and creating a process for promptly removing access when employees change roles or leave the company.

-

Review and refine your setup quarterly by analyzing which permissions are actually used, identifying bottlenecks in approval workflows, and adjusting role definitions as your business evolves.

When evaluating providers, compare their offerings across critical features:

| Provider Feature | Basic Tier | Professional Tier | Enterprise Tier |

|---|---|---|---|

| Maximum Users | 5-10 | 25-50 | Unlimited |

| Role Customization | Preset roles only | Limited custom roles | Fully customizable RBAC |

| Audit Log Retention | 90 days | 1 year | 7 years |

| Currency Accounts | 3-5 currencies | 10-20 currencies | 30+ currencies |

| API Access | None | Read-only | Full integration |

| Tenant Isolation | Single tenant | Multi-tenant with basic separation | Enterprise-grade isolation |

Streamlining business banking requires choosing a provider whose capabilities match your operational complexity. Smaller SMBs may function well with preset roles and basic multi-currency support, while businesses with multiple entities or complex approval chains need advanced customization.

Ongoing management centers on three practices. First, conduct quarterly access reviews to ensure users still need their assigned permissions and remove access for departed employees immediately. Second, analyze your audit logs monthly to identify unusual patterns, verify that approval workflows function as intended, and spot opportunities to streamline operations. Third, stay current with your provider's feature updates, as international bank account solutions continuously evolve to meet changing regulatory requirements and business needs.

The key to successful implementation is starting simple and expanding gradually. Begin with core roles and basic permissions, then add complexity only when clear operational needs emerge. This approach prevents the overwhelming permission structures that plague organizations trying to account for every possible scenario upfront.

Streamline your business banking operations with Bankz

Managing multi-user access, multiple currencies, and cross-border payments doesn't have to mean juggling multiple banking relationships or wrestling with outdated systems. Bankz provides European SMBs with a comprehensive multi-user business account platform designed specifically for the complexities of international operations.

Our platform offers role-based permissions that you can configure to match your exact organizational structure, from simple setups with a few users to complex hierarchies with department-specific access controls. Built-in audit logs track every action automatically, satisfying compliance requirements while giving you complete visibility into your business finances.

Multi-currency accounts and business debit Visa cards integrate seamlessly, allowing your team to hold balances in dozens of currencies and execute cross-border payments through SEPA, SWIFT, and local payment rails. Whether you're paying suppliers in one country while receiving customer payments in another, Bankz handles the complexity so you can focus on growing your business. The benefits of international business bank accounts become immediately apparent when you can manage everything from a unified dashboard rather than logging into multiple systems.

Frequently asked questions about multi-user business accounts

What is a multi-user business account and how does it improve security?

A multi-user business account allows multiple authorized individuals to access company finances with role-specific permissions rather than sharing login credentials. Security improves through role-based access control that limits each user to only the functions they need, tenant isolation that prevents data leaks between business units, and comprehensive audit logs that track every action with timestamps and user identification.

Can multiple currencies be managed within one multi-user business account?

Yes, modern multi-user business accounts support holding, receiving, and sending funds in dozens of currencies from a single platform. You can maintain separate currency balances, execute cross-border payments through SEPA and SWIFT rails, and provide currency-specific access to different team members based on their operational needs. This eliminates the need for multiple bank accounts in different countries.

How do role-based permissions help in managing business finances?

Role-based permissions allow you to grant each team member exactly the access they need for their job function without exposing them to sensitive areas outside their responsibility. Your accountant can generate reports without initiating payments, your operations team can process supplier transactions without modifying user permissions, and your executives maintain oversight without handling routine tasks. This creates natural checks and balances while accelerating workflow by enabling parallel task execution.

Are multi-user accounts compliant with European cross-border banking regulations?

Multi-user business accounts designed for European markets integrate compliance features directly into their architecture. They support SEPA standards for euro-zone transfers, provide IBAN accounts that meet EU banking requirements, and maintain audit trails that satisfy record-keeping regulations across member states. The built-in documentation and transparency features actually simplify compliance compared to traditional accounts where you must manually track and report activities.

What are the best practices for assigning user roles within the account?

Start with broad role categories like payment initiator, approver, and viewer before creating specialized roles, which prevents permission sprawl. Map roles to job functions rather than individual people, making it easier to onboard new team members or reassign responsibilities. Implement the principle of least privilege by granting only the minimum permissions needed for each role. Review access quarterly to remove unused permissions and departed employees, and use your audit logs to verify that workflows function as intended. Consider exploring international business bank solutions that offer flexible role configuration to match your specific organizational structure.