Virtual business accounts now reduce onboarding time by up to 90% compared to traditional banks, transforming how SMEs and startups manage international finances. These digital-only solutions eliminate physical branch requirements, cut cross-border payment fees dramatically, and enable multi-currency transactions from a single dashboard. This guide walks you through everything you need to know: how virtual accounts work, their security features, practical benefits, and choosing the right provider for your growing business.

Table of Contents

- Understanding Virtual Business Accounts: Definition And Core Functionality

- How Virtual Business Accounts Handle Multi-Currency And Cross-Border Transactions

- Regulatory Landscape And Security Of Virtual Business Accounts

- Benefits Of Virtual Business Accounts For SMEs And Startups

- Common Misconceptions About Virtual Business Accounts

- Comparing Virtual Business Accounts With Traditional Bank Accounts

- How To Choose And Implement A Virtual Business Account

- Explore Bankz Virtual Business Account Solutions

Key takeaways

| Point | Details |

|---|---|

| Speed and efficiency | Virtual business accounts enable 40% higher SME approvals with onboarding in 24-48 hours versus weeks for traditional banks. |

| Cost savings | Multi-currency support and transparent exchange rates reduce cross-border payment fees by up to 70% compared to conventional banking. |

| Compliance and security | Reputable providers partner with licensed institutions and implement PSD2, GDPR compliance, encryption, and two-factor authentication as standard. |

| Selection criteria | Evaluate providers based on fee structures, supported currencies, API integration capabilities, and customer support quality for optimal fit. |

Understanding virtual business accounts: definition and core functionality

A virtual business account is a fully digital banking solution that provides core financial services without physical branches. Unlike traditional banks requiring in-person visits and lengthy paperwork, these accounts operate entirely online through secure platforms and mobile apps. The digital-first approach eliminates geographic constraints and drastically accelerates the account setup process.

Business account verification processes for virtual accounts typically complete in 24-48 hours. Traditional banks often require 2-4 weeks for similar approval. This speed advantage matters critically for startups and SMEs needing immediate access to banking infrastructure to capture market opportunities or manage cash flow.

SMEs and startups form the primary user base for virtual business accounts. These businesses value flexibility, speed, and cost efficiency over in-person banking relationships. Remote companies, cross-border e-commerce operations, and international service providers particularly benefit from virtual account features.

Core features distinguish virtual business accounts from conventional options:

- Complete online management through web dashboards and mobile applications

- Rapid account opening requiring only digital documentation

- Multi-currency account capabilities with multiple IBANs

- Integrated payment processing for SEPA, SWIFT, and local schemes

- Virtual and physical business debit cards for expense management

- API connectivity enabling automation with accounting and payment systems

The operational model differs fundamentally from traditional banking. Virtual account providers partner with licensed financial institutions rather than holding full banking licenses themselves. This structure allows them to offer banking services while focusing on user experience, technology integration, and specialized features for digital-first businesses.

How virtual business accounts handle multi-currency and cross-border transactions

Virtual business accounts solve one of the costliest challenges facing international SMEs: efficient multi-currency management. Traditional banks typically maintain single-currency accounts, forcing businesses to open separate accounts for each currency or accept unfavorable conversion rates on incoming payments. Virtual accounts assign multiple IBANs per currency within a single account structure.

This multi-IBAN architecture means your business receives a dedicated EUR IBAN, GBP IBAN, and USD account details under one account umbrella. Clients paying in EUR send funds directly to your EUR IBAN, eliminating intermediary bank fees and currency conversion charges. The same principle applies across all supported currencies, preserving payment value.

Built-in currency exchange features offer transparency that traditional banks rarely match. Virtual account platforms display real-time exchange rates, explicit conversion fees, and exact amounts you'll receive. Many providers offer rates within 0.5-1% of mid-market rates compared to 3-5% markups common at traditional banks.

International payment scheme support enables true cross-border flexibility:

- SEPA transfers process EUR payments across European Economic Area countries in 1-2 business days

- SWIFT network connectivity facilitates payments to virtually any global bank

- Local payment rails like UK Faster Payments provide same-day GBP transfers

- Bulk payment capabilities allow scheduling multiple international transfers simultaneously

Multi-currency accounts streamline operations by centralizing currency management. Finance teams access all currency balances from a single dashboard rather than logging into multiple bank portals. This consolidation reduces administrative overhead and improves financial visibility.

| Feature | Virtual Business Account | Traditional Bank Account |

|---|---|---|

| Average SEPA transfer time | 1-2 business days | 2-4 business days |

| SWIFT transfer fees | $10-25 per transfer | $35-60 per transfer |

| Currency conversion markup | 0.5-1% above mid-market | 3-5% above mid-market |

| Multi-currency IBAN availability | 5-10 currencies standard | Requires separate accounts |

| Exchange rate transparency | Real-time rates displayed | Rates disclosed after transaction |

The cross-border payment process through virtual accounts follows a streamlined workflow. First, you select the recipient currency and destination country. The platform calculates exact fees and exchange rates before you confirm. Funds debit from your chosen currency balance or convert automatically from another currency at the displayed rate. Recipients receive payments faster because virtual account providers optimize routing through correspondent banking networks.

Regulatory landscape and security of virtual business accounts

Virtual business accounts operate within stringent regulatory frameworks designed to protect businesses and consumers. The revised Payment Services Directive (PSD2) governs payment services across the European Economic Area, establishing security requirements, consumer protection standards, and operational guidelines for both traditional banks and virtual account providers.

Most virtual account providers use one of two regulatory models. Some partner with fully licensed banks that hold the actual customer funds and provide banking infrastructure. Others obtain e-money institution licenses, allowing them to issue electronic money and provide payment services directly while maintaining segregated client fund accounts.

GDPR compliance forms another critical regulatory pillar. Virtual account platforms must implement robust data protection measures, transparent privacy policies, and secure data processing procedures. These requirements actually benefit users by mandating clear communication about data usage and strong security protocols.

Security measures implemented by reputable virtual account providers typically exceed those of traditional banks in several areas:

- AES 256-bit encryption protects data transmission and storage

- Two-factor authentication (2FA) requires multiple verification methods for account access

- Real-time fraud monitoring systems flag suspicious transactions immediately

- Role-based access controls limit which team members can authorize payments

- Device fingerprinting and IP monitoring detect unauthorized access attempts

- Automated alerts notify account holders of significant transactions instantly

Common security myths deserve clarification. Virtual accounts are not inherently less secure than traditional bank accounts. Regulated virtual account providers implement the same encryption, authentication, and monitoring technologies as major banks. The digital-only model actually reduces certain risks like lost paper statements or intercepted physical mail.

The deposit protection landscape varies by provider structure. Virtual accounts partnered with EU banks may offer deposit insurance up to €100,000 per depositor through national schemes. E-money institutions must safeguard client funds in segregated accounts at licensed banks, protecting deposits even if the provider faces financial difficulties.

Pro Tip: Before selecting a virtual account provider, verify their regulatory status through official registries. Check whether they hold an e-money license, operate as a payment institution, or partner with a licensed bank. Confirm their compliance with PSD2 and GDPR through published certifications and security documentation.

Benefits of virtual business accounts for SMEs and startups

The speed advantage of virtual business accounts transforms business launch timelines. Onboarding completes in 24-48 hours for most SMEs, compared to 2-4 weeks at traditional banks. This acceleration allows startups to receive investor funds, pay suppliers, and begin operations immediately rather than delaying business activities while waiting for banking access.

Cost efficiency extends beyond faster onboarding. Virtual accounts eliminate monthly maintenance fees common at traditional banks, which often charge $15-50 per month for business accounts. International payment fees drop dramatically, with virtual providers charging $10-25 per SWIFT transfer versus $35-60 at conventional banks. These savings compound quickly for businesses making regular cross-border payments.

Currency conversion represents another major cost advantage. Traditional banks typically add 3-5% markups to exchange rates, meaning a $10,000 currency conversion costs $300-500 in hidden fees. Virtual accounts offer rates within 0.5-1% of mid-market rates, reducing the same conversion cost to $50-100. For businesses processing substantial international revenue, annual savings reach thousands or tens of thousands of dollars.

Automation capabilities distinguish modern virtual account platforms. API integrations connect your account with accounting software like QuickBooks, Xero, or custom finance systems. Transactions sync automatically, eliminating manual data entry and reducing accounting errors. Payment processing integrates with e-commerce platforms, enabling automatic invoice reconciliation.

Virtual and physical business debit cards provide spending flexibility that enhances expense management:

- Issue unlimited virtual cards for online subscriptions and digital advertising spend

- Generate single-use virtual cards for vendor payments to limit fraud exposure

- Provide physical cards to team members with customizable spending limits

- Track expenses in real-time through the account dashboard

- Block or freeze cards instantly if lost or compromised

- Set merchant category restrictions to control spending types

The virtual IBAN system enables sophisticated payment collection strategies. Assign unique IBANs to different clients, revenue streams, or business units while maintaining a single consolidated account. This structure simplifies reconciliation, improves cash flow visibility, and automates accounting processes without requiring multiple separate accounts.

Reporting and analytics features provide financial insights that traditional banks rarely offer. Virtual account dashboards visualize spending patterns, track currency exposure, and forecast cash flow based on pending transactions. Export capabilities allow seamless data transfer to financial planning tools for deeper analysis.

Pro Tip: Leverage API connectivity to build automated workflows that trigger actions based on account activity. Configure systems to send alerts when balances fall below thresholds, automatically convert currencies when rates hit targets, or generate invoices when payments arrive. These automations reduce manual monitoring and free finance teams to focus on strategic activities.

Common misconceptions about virtual business accounts

Myth: Virtual accounts are less secure than traditional banks. Reality: Reputable virtual account providers implement identical security protocols to major banks, including encryption, two-factor authentication, and fraud monitoring. Regulatory requirements ensure security standards match or exceed traditional banking. The digital-only model actually eliminates certain physical security risks like stolen checkbooks or intercepted mail.

Myth: Virtual accounts lack regulatory oversight. Reality: Virtual business account providers must comply with PSD2, GDPR, and national financial regulations. They either hold e-money licenses issued by financial regulators or partner with fully licensed banks. Regulatory authorities supervise these providers as strictly as traditional banks, conducting regular audits and enforcing compliance.

Myth: Customer support is poor or non-existent. Reality: Many virtual account providers offer superior support compared to traditional banks. Support teams specialize in SME needs and digital banking questions. Response times often beat traditional banks, with email support answering within hours and chat support providing real-time assistance. Some providers assign dedicated account managers to business clients, offering personalized guidance.

Myth: Only tech-savvy businesses can use virtual accounts effectively. Reality: Modern virtual account platforms prioritize user experience and accessibility. Interfaces mirror familiar banking apps with intuitive navigation and clear labeling. Onboarding wizards guide users through setup step-by-step. Educational resources, video tutorials, and responsive support teams help non-technical users master platform features quickly. Small businesses without dedicated IT staff successfully manage virtual accounts daily.

Myth: Virtual accounts cannot handle complex business banking needs. Reality: Virtual business accounts support sophisticated financial operations including multi-currency management, bulk payments, API integrations, and automated reconciliation. Many providers offer features traditional banks lack, such as unlimited virtual cards, real-time currency conversion, and programmable payment workflows. Businesses with complex international operations often find virtual accounts more capable than conventional banking.

Myth: Funds in virtual accounts are not protected. Reality: Deposit protection depends on the provider's regulatory structure. Virtual accounts partnered with EU banks typically offer deposit insurance up to €100,000 per depositor. E-money institutions must safeguard client funds in segregated accounts at licensed banks, ensuring protection even if the provider encounters financial difficulties. Always verify the specific protection mechanism your chosen provider uses.

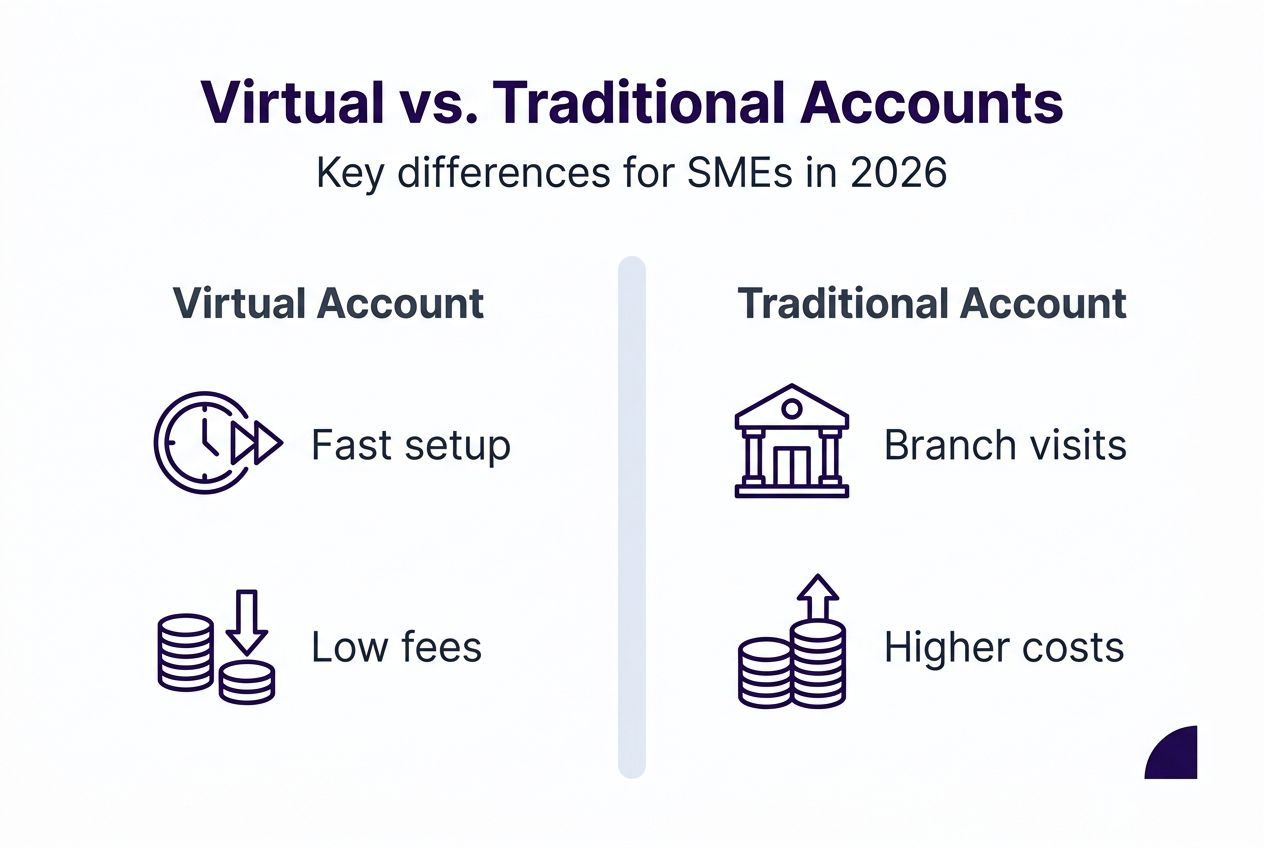

Comparing virtual business accounts with traditional bank accounts

Choosing between virtual and traditional business accounts requires understanding how each performs across critical criteria. The comparison reveals distinct strengths and ideal use cases for each account type.

Fees and transparency represent a primary differentiator. Virtual accounts typically charge no monthly maintenance fees and offer transparent pricing published clearly on their websites. Transaction fees are lower, particularly for international payments. Traditional banks often bundle fees in complex pricing tiers, making true costs difficult to calculate until charges appear on statements.

| Criteria | Virtual Business Account | Traditional Bank Account |

|---|---|---|

| Monthly maintenance fee | $0-10 | $15-50 |

| Account opening time | 24-48 hours | 2-4 weeks |

| Multi-currency IBANs | 5-10 currencies standard | Requires separate accounts |

| International transfer fees | $10-25 per SWIFT payment | $35-60 per SWIFT payment |

| Currency conversion markup | 0.5-1% above mid-market | 3-5% above mid-market |

| API integration | Standard feature | Rare or expensive add-on |

| Virtual card issuance | Unlimited, instant | Limited or unavailable |

| Customer support | Email, chat, often 24/7 | Branch visits, phone during business hours |

Onboarding and transaction speed favor virtual accounts decisively. Digital verification processes approve accounts in 1-2 days versus weeks at traditional banks. Digital banking solutions process payments faster because they optimize routing through modern correspondent networks.

Multi-currency support shows the starkest contrast. Virtual accounts provide 5-10 currency IBANs within a single account structure. Traditional banks require opening separate accounts for each currency, multiplying administrative burden and fees. This difference matters critically for businesses managing international revenue streams.

Customer service models differ fundamentally. Traditional banks offer in-person branch support but often during limited hours. Virtual account providers deliver responsive email and chat support, frequently 24/7. The trade-off: no face-to-face meetings versus faster response times and specialized digital banking expertise.

Operational flexibility advantages virtual accounts for remote and international businesses. Access your account from anywhere with internet connectivity. No branch visits means no geographic constraints. Traditional banks may restrict access or require physical presence for certain transactions, creating friction for distributed teams.

Ideal scenarios for choosing virtual business accounts:

- Startups needing immediate banking access to begin operations

- Remote-first companies without physical headquarters

- E-commerce businesses processing international payments

- SMEs making frequent cross-border transfers

- Companies requiring API integration with accounting or payment systems

- Businesses seeking to minimize banking fees and maximize transparency

When traditional bank accounts make more sense:

- Established businesses with complex credit needs requiring business loans

- Companies regularly depositing large amounts of cash

- Businesses requiring merchant services deeply integrated with banking

- Organizations prioritizing in-person relationship banking

- Industries where clients specifically request traditional bank references

Many successful businesses use both account types strategically. Maintain a traditional bank account for core operations and credit relationships while using a virtual account for international payments and currency management. This hybrid approach optimizes for both relationship banking and operational efficiency.

How to choose and implement a virtual business account

Selecting and implementing the right virtual business account requires a systematic evaluation process. Following these steps ensures you choose a provider that matches your business needs and integrates smoothly with existing operations.

Step 1: Identify your specific banking requirements. List the currencies you regularly transact in and payment methods you need. Calculate your monthly transaction volume and typical transfer amounts. Determine whether you need API integration with existing software. Understanding requirements upfront focuses your provider search on compatible options.

Step 2: Evaluate provider compliance and security credentials. Verify regulatory status through official financial authority registries. Confirm PSD2 and GDPR compliance through published certifications. Check whether the provider holds an e-money license or partners with a licensed bank. Review security documentation describing encryption standards, authentication methods, and fraud monitoring systems.

Step 3: Compare onboarding processes and user reviews. Research typical approval times and required documentation. Read reviews from businesses similar to yours on independent platforms. Evaluate the user interface through demo videos or free trials. Fast onboarding matters less if the platform proves difficult to use daily.

Step 4: Assess technology integration capabilities. Confirm API availability and documentation quality if you plan to automate workflows. Verify compatibility with your accounting software, e-commerce platform, or payment processors. Test whether the provider offers webhooks for real-time transaction notifications. Strong integration capabilities multiply efficiency gains.

Step 5: Analyze complete fee structures for your usage patterns. Request detailed pricing covering monthly fees, transaction charges, currency conversion rates, and card issuance costs. Calculate total monthly costs based on your projected transaction volume. Compare at least three providers to identify the best value. Remember that lowest fees don't always indicate best overall value.

Step 6: Test customer support responsiveness before committing. Contact support with detailed questions about features relevant to your business. Evaluate response time, knowledge depth, and communication quality. Support quality matters critically when issues arise or you need guidance implementing new features.

Implementation follows a structured path once you've selected a provider. Gather required documentation including business registration, ownership identification, and proof of address. Complete the online application accurately to avoid delays. Upload clear, high-resolution document scans. Most approvals complete within 24-48 hours if documentation is complete.

After approval, configure account settings to match your operational needs. Set up multi-currency wallets for relevant currencies. Order physical cards for team members who need them. Generate virtual cards for online subscriptions and vendor payments. Configure spending limits and merchant restrictions to control expenses.

Integrate the account with existing systems to maximize efficiency. Connect API endpoints to your accounting software for automatic transaction sync. Link payment processors to your international business account for streamlined collection. Set up automated currency conversion rules if you regularly exchange currencies.

Train your team on platform features and workflows. Create documentation for common tasks like initiating payments, reconciling transactions, and generating reports. Schedule onboarding sessions with your account manager if available. Ensure all authorized users understand security protocols including 2FA and device verification.

Pro Tip: Avoid selecting a provider based solely on having the lowest fees. Balance cost considerations with feature completeness, regulatory compliance, and support quality. A provider charging slightly higher fees but offering superior API integration and responsive support often delivers better long-term value than the cheapest option with limited capabilities.

Explore Bankz virtual business account solutions

Now that you understand how virtual business accounts transform international banking for SMEs, Bankz offers comprehensive solutions designed specifically for your needs. Our platform provides multi-currency accounts with rapid onboarding, typically completing in 24-48 hours, allowing you to start managing international finances immediately.

Bankz multi-currency accounts and business Visa cards support seamless cross-border payments through SEPA, SWIFT, and local payment rails. Competitive currency exchange rates and transparent fee structures reduce your international payment costs significantly. API integration capabilities connect your Bankz account with accounting software and payment systems, automating workflows and eliminating manual data entry. Both virtual and physical business debit cards provide flexible expense management for your team.

Explore Bankz solutions to discover how our virtual business account platform can streamline your international banking operations and accelerate your business growth.

FAQ

What is a virtual business account?

A virtual business account is a fully digital banking solution that provides core financial services without physical branches. It enables SMEs and startups to manage multi-currency transactions, make international payments, and handle business banking entirely online. Virtual accounts offer faster onboarding and more flexible features than traditional banks.

How do virtual business accounts reduce international payment costs?

Virtual accounts assign multiple currency IBANs that allow receiving payments directly without intermediary bank fees. They offer currency exchange at rates within 0.5-1% of mid-market compared to 3-5% markups at traditional banks. Transparent pricing and optimized payment routing further reduce hidden costs that conventional banks often charge.

Are virtual business accounts secure and regulated?

Yes, reputable virtual account providers comply with PSD2 and GDPR regulations while partnering with licensed banks or holding e-money institution licenses. They implement bank-grade security including AES 256-bit encryption, two-factor authentication, and real-time fraud monitoring. Regulatory oversight ensures virtual accounts meet the same security standards as traditional banks.

Can all small businesses use virtual business accounts?

Yes, virtual business accounts are designed for accessibility across all SME types regardless of technical expertise. User-friendly interfaces, guided onboarding processes, and responsive customer support make these accounts simple to use. Businesses from startups to established SMEs successfully manage virtual accounts without specialized technical skills or dedicated IT teams.