Many SMEs believe traditional banks remain the safest choice for international business banking. This misconception costs companies thousands annually in hidden fees and inefficient cross-border processes. Managing multi-currency accounts and international transactions through legacy banks creates unnecessary complexity and expense. Digital business banking offers European SMEs and online entrepreneurs a more efficient, cost-effective solution in 2026. This article explains why switching to digital platforms can transform your international financial operations and strengthen your competitive position.

Table of Contents

- The Challenges Of Traditional Business Banking For International Smes

- How Digital Business Banking Solves Cross-Border And Multi-Currency Challenges

- Essential Features Of Leading Digital Business Banking Platforms For Smes

- What The Digital Euro Means For The Future Of Business Banking In Europe

- Explore Streamlined Business Banking Solutions With Bankz

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Cost reduction | Digital banks eliminate hidden FX margins and reduce international transfer fees significantly |

| Speed advantage | Cross-border payments process faster through modern digital infrastructure than legacy systems |

| Integration benefits | Seamless connections with accounting software reduce manual errors and save administrative time |

| Multi-currency infrastructure | Holding multiple currencies simultaneously is essential for efficient international business operations |

| Provider selection impact | Your choice of digital bank directly affects working capital management and compliance risk |

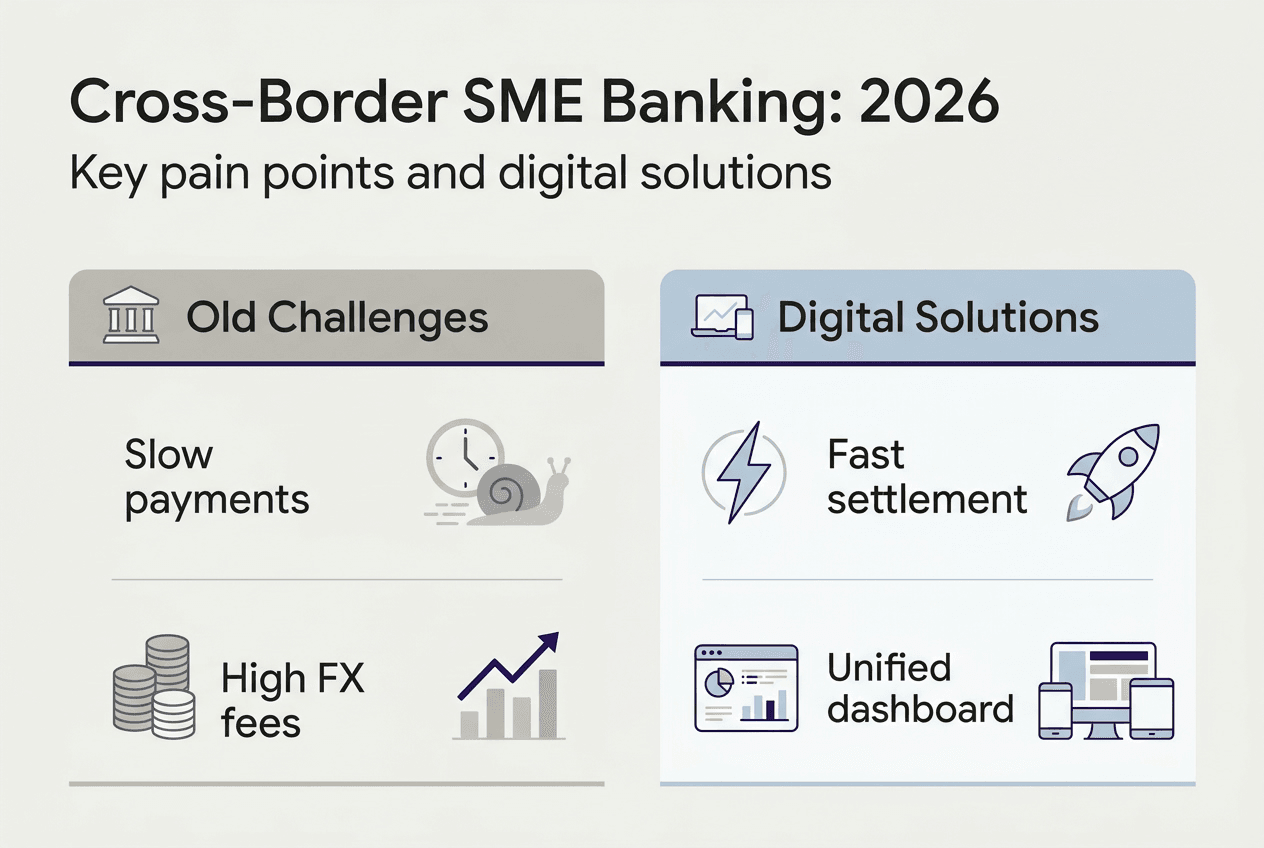

The challenges of traditional business banking for international SMEs

Traditional banks create substantial obstacles for businesses operating across borders. Choosing the right digital business bank can impact working capital, FX exposure, and compliance risk, yet many SMEs remain unaware of how much their current banking arrangements cost them. Legacy institutions charge hidden fees that erode profit margins without providing corresponding value.

The inefficiencies extend beyond simple transaction costs. Cross-border payments through traditional banks take days to process, tying up working capital when businesses need it most. Currency conversions happen at unfavorable rates with spreads that can reach 3% or higher. These costs compound quickly for companies making regular international payments.

Several specific pain points characterize traditional banking for international operations:

- Hidden FX margins add 2-3% to every currency conversion without transparent disclosure

- International wire transfers take 3-5 business days compared to same-day digital alternatives

- Monthly account fees stack up when maintaining separate accounts in different currencies

- Limited integration with modern accounting software creates manual reconciliation work

- Compliance support remains generic rather than tailored to multi-currency business needs

Working capital suffers dramatically under these conditions. When payments sit in processing limbo for days, businesses cannot reinvest those funds or meet immediate obligations. The opportunity cost alone justifies exploring digital banking advantages for businesses that eliminate these delays.

Legacy payment infrastructure struggles with emerging requirements like digital euro compatibility and real-time settlement systems. Banks built on decades-old technology cannot simply flip a switch to modernize. This technological debt creates ongoing friction for businesses that need agility in their financial operations. Traditional institutions also lack the specialized features international SMEs require, treating cross-border transactions as occasional exceptions rather than core business activities.

Pro Tip: Calculate your actual FX costs by comparing the exchange rate your bank charges against the mid-market rate on the same day. The difference reveals your true conversion expense.

How digital business banking solves cross-border and multi-currency challenges

Digital business banks eliminate the structural problems plaguing traditional international banking. Digital business banks offer significant cost savings compared to traditional banks, particularly for cross-border transactions, with some platforms reducing FX costs by 80% or more. These savings translate directly to improved bottom lines for SMEs operating internationally.

Multi-currency wallets represent the cornerstone feature addressing international business needs. Instead of maintaining separate accounts in different countries, businesses hold multiple currencies within a single platform. Multi-currency accounts are often cheaper than traditional banks because they remove hidden FX margins and international transfer fees, allowing companies to receive payments in local currencies and convert only when rates favor them.

The cost advantages extend across several dimensions:

- FX spreads drop to 0.3-0.8% compared to 2-3% at traditional banks

- International transfers complete in hours rather than days, improving cash flow

- Zero monthly fees for basic multi-currency account maintenance in many cases

- Transparent pricing models show exact costs before confirming transactions

- Batch payment capabilities reduce per-transaction expenses for high-volume operations

Speed and flexibility transform how businesses manage international payments. Same-day settlement becomes standard rather than exceptional. Companies can schedule payments to optimize exchange rates or meet specific supplier deadlines. The multi-currency account benefits include holding funds in anticipation of favorable rate movements rather than converting immediately at unfavorable spreads.

Digital platforms bundle features that traditional banks charge separately. Corporate cards link directly to multi-currency accounts, allowing team members to spend in local currencies without conversion fees. FX management tools provide rate alerts and automated conversions at target levels. Integration with accounting software like QuickBooks and Xero eliminates manual transaction entry and reconciliation work.

| Provider Type | Average FX Spread | Transfer Speed | Monthly Fee | Accounting Integration |

|---|---|---|---|---|

| Traditional Bank | 2.5-3.0% | 3-5 days | $25-50 | Limited |

| Digital Business Bank | 0.4-0.8% | Same day | $0-15 | Native |

| Specialized Fintech | 0.3-0.6% | Hours | $0-10 | API Available |

The ability to manage international business accounts from a unified dashboard reduces administrative overhead significantly. Finance teams spend less time tracking transactions across multiple platforms and more time on strategic activities. Real-time visibility into all currency positions enables better cash management decisions.

Pro Tip: Set up rate alerts for your most common currency pairs to convert funds automatically when favorable rates appear, maximizing your working capital efficiency.

Essential features of leading digital business banking platforms for SMEs

Selecting the right digital business bank requires evaluating specific capabilities that directly impact operational efficiency. Digital business banks offer multi-currency wallets, corporate cards, FX tools, and accounting integrations as standard features, but implementation quality varies significantly across providers.

Multi-currency wallets must support the specific currencies your business uses regularly. Leading platforms offer 20-30 currencies with local IBANs for major markets. This capability allows you to receive payments as a local entity, avoiding international transfer fees for your customers and partners. The wallet should display real-time balances across all currencies with instant conversion options.

Corporate card programs provide spending control and transparency that traditional business credit cards cannot match. Virtual cards can be generated instantly for specific vendors or campaigns with predetermined spending limits. Physical cards work globally without foreign transaction fees when linked to appropriate currency balances. Spending categorization happens automatically, feeding directly into expense management systems.

Key features to prioritize include:

- Multi-currency IBAN accounts for receiving payments in local formats

- Real-time FX rates with transparent spread disclosure before conversion

- API access for custom integrations with existing business systems

- Role-based access controls for team members with different responsibilities

- Automated reconciliation that matches transactions to invoices and receipts

FX management tools separate sophisticated platforms from basic offerings. Rate alerts notify you when target exchange rates become available. Forward contracts lock in rates for future transactions, eliminating uncertainty in international deals. Some platforms offer dynamic currency hedging that automatically protects against adverse movements while capturing favorable ones.

Businesses should prioritize platforms that offer seamless integration with their preferred accounting tools to streamline financial operations, reducing errors and saving hours of manual work weekly. Native integrations work better than third-party connectors, providing real-time data synchronization rather than delayed batch updates. The platform should push transaction data directly into your accounting system with proper categorization and currency handling.

Compliance support becomes critical for businesses operating across multiple jurisdictions. Your digital bank should provide documentation that satisfies tax authorities in all relevant countries. Automated reporting for VAT, GST, and other international tax obligations saves significant accounting time. Some platforms offer dedicated compliance teams familiar with cross-border business requirements.

Pro Tip: Before committing to a platform, test its integration with your existing accounting software using a trial account to ensure data flows correctly and reduces rather than increases your administrative workload.

When evaluating providers, request demonstrations showing actual workflows for your specific use cases. Generic feature lists miss nuances that matter in daily operations. Consider opening business account Europe requirements and how different platforms handle verification and onboarding for international companies. Review the business account setup checklist to ensure you gather necessary documentation efficiently.

What the digital euro means for the future of business banking in Europe

The digital euro represents the most significant change to European payment infrastructure in decades. Financial institutions will need to adapt their existing payment infrastructures to the new requirements at an early stage to maintain competitive positions and serve business clients effectively. This transition creates both challenges and opportunities for SMEs managing cross-border operations.

The planned architecture of the digital euro positions banks and other payment service providers as central intermediaries for both payers and payees in transactions. Banks must develop new technical capabilities to facilitate digital euro transfers while maintaining existing payment rails. The dual infrastructure period will require sophisticated systems that handle traditional and digital currency transactions seamlessly.

Implementation timelines remain fluid, but businesses should prepare now rather than scrambling during rollout. Early adoption provides competitive advantages in customer experience and operational efficiency. Companies that integrate digital euro capabilities first will offer superior payment options to European partners and customers.

SMEs should take these specific steps to position themselves advantageously:

- Evaluate your current banking provider's digital euro readiness and implementation timeline

- Assess how digital euro transactions might reduce costs compared to current SEPA transfers

- Consider the compliance implications of holding and transacting in digital euros across jurisdictions

- Review your accounting systems' capability to handle digital currency alongside traditional currencies

- Monitor regulatory developments that might create new reporting requirements for digital euro usage

- Plan technology upgrades needed to accept digital euro payments from customers

The digital euro will likely reduce transaction costs and settlement times even further than current digital banking solutions. Instant settlement becomes guaranteed rather than dependent on banking hours or intermediary processing. This improvement benefits businesses with tight cash flow management needs or those making frequent small-value international payments.

Interoperability requirements mean your digital bank must connect seamlessly with other European financial institutions regardless of their underlying technology. Choosing providers investing heavily in European banking benefits non-EU businesses positions your company to leverage these network effects as the digital euro ecosystem matures.

Security and privacy considerations differ significantly from traditional electronic payments. The digital euro incorporates privacy protections while maintaining anti-money laundering compliance. Understanding these nuances helps businesses communicate payment options effectively to customers concerned about financial privacy.

Explore streamlined business banking solutions with Bankz

Navigating the shift to digital business banking requires partners who understand international SME needs. Bankz provides multi-currency accounts specifically designed for businesses managing cross-border transactions efficiently. The platform eliminates the complexity and excessive costs that plague traditional international banking relationships.

Our international business bank accounts support the currencies you actually use with transparent FX rates and same-day settlement capabilities. Combined with business debit Visa cards that work globally without foreign transaction fees, Bankz delivers the complete digital banking infrastructure modern SMEs require. The integrated dashboard provides real-time visibility across all accounts and currencies, simplifying financial management significantly.

Pro Tip: Evaluate how much you currently spend on international banking fees and FX spreads annually, then compare against Bankz's transparent pricing to quantify potential savings before making the switch.

Frequently asked questions

Is digital business banking safe for handling international payments?

Digital business banks comply with the same strict European financial regulations as traditional institutions, including PSD2 and GDPR requirements. They implement bank-level encryption, multi-factor authentication, and continuous transaction monitoring to detect fraud. Choosing licensed and regulated digital banks ensures your international payments receive the same legal protections as traditional banking, often with superior security technology.

How do multi-currency accounts reduce costs for SMEs?

Multi-currency accounts eliminate the need to convert funds every time you receive or send international payments. You avoid repeated conversion fees by holding balances in various currencies until you need them. These accounts remove hidden FX margins that traditional banks add to exchange rates, potentially saving 2-3% on every transaction. Direct payments in local currencies also reduce intermediary bank charges that stack up with correspondent banking networks.

What integration features should I prioritize in a digital business bank?

Prioritize platforms offering native integration with your accounting software like QuickBooks, Xero, or SAP to eliminate manual data entry. Look for API access that allows custom integrations with your existing financial technology stack. Real-time data synchronization matters more than batch updates for accurate financial visibility. Ensure the platform supports automated reconciliation that matches transactions to invoices without manual intervention.

How quickly can I set up a digital business bank account?

Most digital business banks complete account setup within 24-48 hours once you submit required documentation. The process involves identity verification, business registration confirmation, and compliance checks that happen largely automatically. Some platforms offer instant provisional access while final verification completes in the background. This speed contrasts sharply with traditional banks that often require weeks and in-person meetings for international business accounts.

Will switching to digital banking disrupt my current operations?

Reputable digital banks provide migration support to minimize disruption during the transition period. You can run accounts in parallel initially, gradually shifting payment flows as you gain confidence. Most platforms offer dedicated onboarding specialists who help configure integrations and train your team. The switch typically improves rather than disrupts operations by eliminating manual processes and providing better visibility into international transactions.