Manual cross-border payments cost European SMEs 12 times more outside SEPA zones, yet most businesses still rely on outdated correspondent banking networks that take days to settle transactions. Business banking automation transforms these inefficient processes through intelligent technology that handles repetitive tasks, reduces errors, and accelerates international payments. This guide explains what business banking automation entails, how it specifically benefits SMEs managing cross-border operations in Europe, and practical steps to implement automation successfully in your organization.

Table of Contents

- Understanding Business Banking Automation And Its Core Components

- The Impact Of Automation On Cross-Border SME Banking In Europe

- Navigating Challenges: Handling Exceptions And Achieving High Automation Rates

- Steps For European SMEs To Adopt Business Banking Automation Successfully

- Discover Bankz Solutions To Streamline Your Business Banking In 2026

Key takeaways

| Point | Details |

|---|---|

| Core automation technologies | RPA, BPM, and AI work together to automate account opening, payments, reconciliation, and compliance processes |

| Cross-border efficiency gains | Automated fintech solutions reduce transaction costs and enable instant multi-currency payments compared to traditional banking |

| Exception management matters | Hybrid AI-human systems achieve 90% automation rates by intelligently handling edge cases that consume 3-5x resolution time |

| Phased adoption strategy | Start with high-volume rule-based tasks, then integrate APIs and AI for predictive analytics and exception handling |

| Measurable ROI indicators | Track full-time equivalent savings, processing time reductions, and error rate improvements to quantify automation benefits |

Understanding business banking automation and its core components

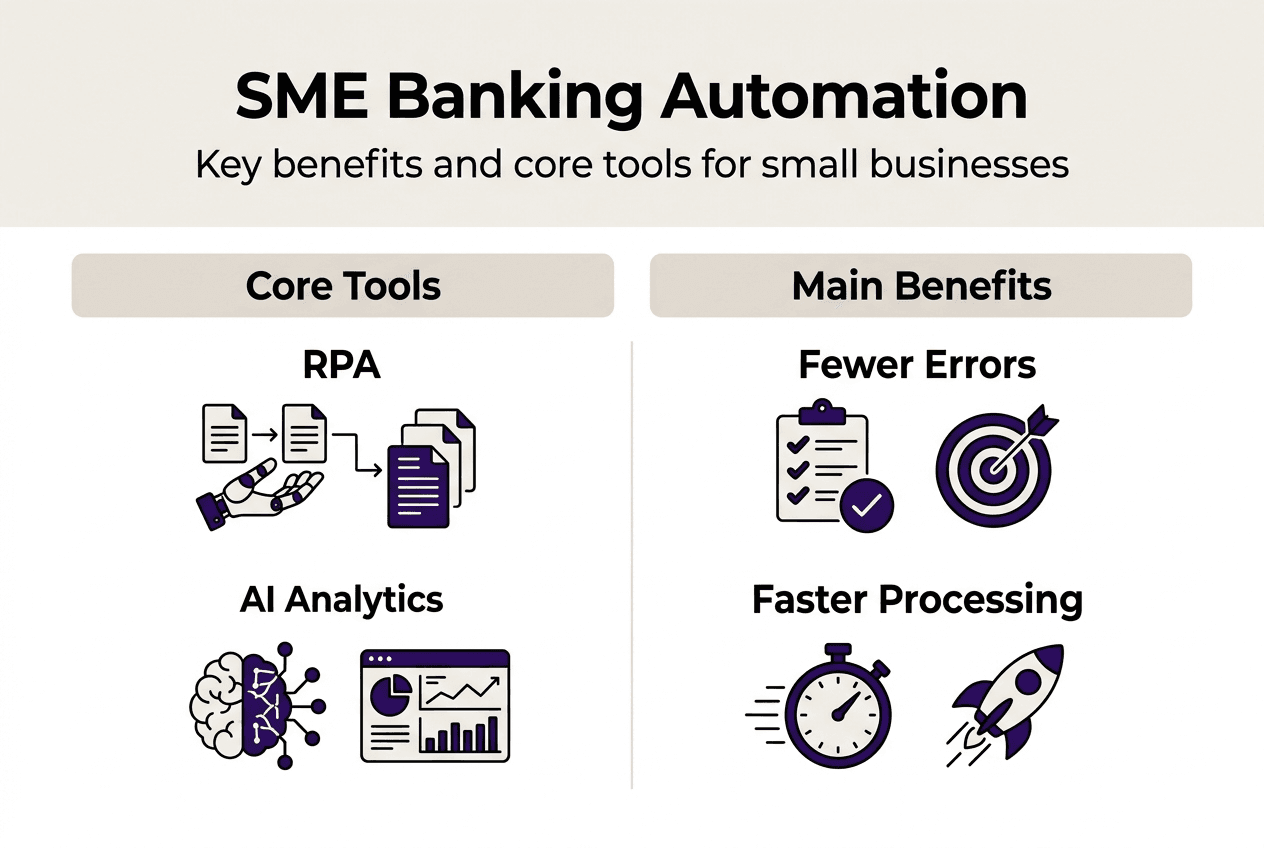

Business process automation in banking refers to technologies like robotic process automation (RPA), business process management (BPM), and artificial intelligence that automate complex banking processes for businesses. The goal is eliminating manual intervention in repetitive tasks while maintaining accuracy and regulatory compliance. For SMEs handling cross-border transactions, this means faster payments, reduced operational costs, and fewer human errors in critical financial workflows.

Core technologies powering automation include RPA for rule-based tasks, BPM for workflow orchestration, and AI for pattern recognition and decision-making. IBM business process automation systems use workflow orchestration through BPMN standards, decision automation via DMN frameworks, and API integrations to connect disparate banking systems. Agentic AI represents the latest evolution, enabling systems to make autonomous decisions within defined parameters for complex scenarios like payment exceptions or fraud detection.

Automation impacts multiple banking processes that SMEs use daily. Account opening workflows verify identity documents and business registration automatically. Payment processing routes transactions through optimal channels based on currency, destination, and cost. Reconciliation matches incoming payments with invoices without manual data entry. KYC and AML compliance checks run continuously in the background. Cross-border transactions benefit most dramatically, as automation selects the fastest, cheapest routing options across SEPA, SWIFT, and local payment networks.

AI enhances automation through pattern recognition in transaction matching, achieving 90-95% accuracy rates that surpass manual processing. Machine learning models predict cash flow needs, identify anomalies indicating fraud, and optimize currency exchange timing. For digital business banking cross-border operations, this intelligence layer transforms basic automation into a strategic advantage.

Key components and technologies include:

- Workflow orchestration engines managing multi-step processes across systems

- Decision automation frameworks applying business rules consistently

- API integrations connecting banking platforms with accounting and ERP software

- Machine learning models for predictive analytics and anomaly detection

- Robotic process automation handling data entry and validation tasks

Benefits extend beyond time savings. Error rates drop dramatically when systems validate data automatically. Processing speed increases from days to minutes for routine transactions. Compliance becomes continuous rather than periodic. Staff focus shifts from data entry to strategic financial management. Understanding types of business bank accounts helps SMEs choose platforms with robust automation capabilities built in.

The impact of automation on cross-border SME banking in Europe

Automation fundamentally changes how European SMEs manage international banking operations. SEPA payments and multi-currency accounts become accessible through automated platforms that previously required complex correspondent banking relationships. Instead of manually initiating wire transfers and tracking exchange rates, businesses set rules that execute payments automatically when invoices are due or favorable FX rates appear.

Cost differences between traditional and automated approaches are substantial. Cross-border transactions outside SEPA zones cost 12 times more through traditional correspondent banking networks compared to automated fintech solutions. Fintechs provide instant payments, real-time currency conversion, and transparent fee structures that eliminate hidden intermediary charges. For SMEs processing dozens of international transactions monthly, these savings compound quickly into significant annual cost reductions.

| Metric | Traditional Correspondent Banking | Automated Fintech Solutions |

|---|---|---|

| Average transaction time | 3-5 business days | Minutes to hours |

| Cross-border fees | 3-5% plus intermediary charges | 0.5-1.5% transparent fees |

| Currency conversion markup | 3-4% above interbank rates | 0.3-0.8% above interbank rates |

| Manual reconciliation time | 2-4 hours per day | Automated real-time matching |

| Payment tracking visibility | Limited, requires bank inquiries | Real-time status updates |

Automation delivers specific operational benefits for European SMEs. Lower transaction fees directly improve margins on international sales. Faster FX hedging capabilities protect against currency volatility when quotes are issued in foreign currencies. Improved invoice processing matches payments to receivables automatically, reducing days sales outstanding. Multi-currency holding accounts eliminate conversion costs when revenues and expenses occur in the same foreign currency.

Pro Tip: Prioritize automating your highest-volume processes first, such as payment reconciliation and routine SEPA transfers, to achieve quick wins that build internal support for broader automation initiatives.

Fintechs like WorldFirst and wamo demonstrate how automation serves European SMEs effectively. These platforms integrate multi-currency banking cost reduction features with automated payment routing that selects optimal channels based on destination, amount, and urgency. Real-time dashboards provide visibility into cash positions across currencies without manual consolidation. API connections sync transaction data with accounting software automatically, eliminating duplicate data entry and reconciliation errors.

Streamlining international banking with SEPA and IBAN becomes seamless when automation handles the technical complexity. Systems validate IBANs before initiating transfers, check beneficiary details against sanctions lists, and route payments through the most cost-effective networks automatically. This level of sophistication was previously available only to large corporations with dedicated treasury teams.

Navigating challenges: handling exceptions and achieving high automation rates

Exception cases represent the frontier where automation either succeeds or stalls. Common edge cases include data mismatches between invoice and payment references, partial payments requiring manual allocation decisions, lost or corrupted transaction data, regulatory differences across jurisdictions, and business logic conflicts when rules produce ambiguous outcomes. These scenarios don't fit standard automation rules and historically required human intervention.

Exceptions consume disproportionate resources. Studies show 40-60% of cases become exceptions requiring 3-5 times longer resolution time than standard transactions. When automation handles only straightforward cases, the efficiency gains diminish as staff spend increasing time on the remaining complex scenarios. This creates a ceiling where automation rates plateau around 50-60% despite significant technology investment.

Advanced exception management strategies push automation rates higher. Exception orchestration systems route edge cases to appropriate resolution workflows based on exception type and complexity. Fingerprinting uses pattern recognition to identify similar past exceptions and apply proven resolution approaches automatically. Hybrid AI-human decision loops present exceptions to staff with recommended actions based on historical data, reducing decision time while maintaining human oversight for critical judgments.

"Exception handling represents the hidden cost center in B2B payments, where manual intervention on edge cases erodes the efficiency gains from automating standard transactions, making sophisticated exception management the key differentiator for achieving true straight-through processing rates above 90%."

Agentic AI revolutionizes payment exceptions by applying cognitive reasoning to ambiguous scenarios. These systems analyze context, evaluate multiple resolution options, predict outcomes, and execute decisions autonomously within defined risk parameters. For cross-border payments, agentic AI resolves currency mismatches, incomplete beneficiary data, and routing conflicts without human intervention while flagging truly novel situations for review.

Practical approaches to improve exception handling include:

- Implement exception categorization that routes cases by complexity and risk level

- Build knowledge bases capturing resolution patterns from historical exceptions

- Use machine learning to predict which transactions will become exceptions before processing

- Create escalation workflows with clear decision authority at each level

- Monitor exception rates by type to identify process improvements that prevent exceptions

- Establish feedback loops where resolved exceptions train AI models for future automation

Pro Tip: Focus your automation maturity efforts on exception orchestration rather than just adding more rules, as sophisticated exception handling drives automation success rates from 60% to 90% more effectively than expanding rule-based RPA coverage.

Risks accompany agentic AI adoption. Autonomous systems making financial decisions require robust governance frameworks, clear accountability structures, and continuous monitoring. Start with narrow use cases where decision impacts are limited and expand gradually as confidence builds. Digital business banking platforms increasingly embed these capabilities, but SMEs must understand the technology's limitations and maintain appropriate human oversight.

Steps for European SMEs to adopt business banking automation successfully

Phased implementation manages risks while delivering incremental value. Follow this roadmap:

- Audit existing banking processes to identify high-volume, rule-based tasks consuming staff time and prone to errors

- Automate straightforward processes first, such as payment initiation, invoice matching, and account reconciliation using RPA tools

- Integrate open banking APIs to connect your banking platform with accounting software, ERP systems, and payment gateways

- Add AI capabilities for exception handling, predictive cash flow analytics, and fraud detection as automation matures

- Continuously monitor performance metrics, gather user feedback, and optimize workflows based on actual usage patterns

| Aspect | Traditional Banking Processes | Phased Automated Approach |

|---|---|---|

| Initial setup effort | Low, manual processes require minimal technology | Moderate, requires process mapping and tool selection |

| Ongoing operational cost | High, significant staff time on repetitive tasks | Low, automated execution with exception management |

| Error rates | 2-5% due to manual data entry and fatigue | Under 0.5% with validation and automated checks |

| Scalability | Limited, adding volume requires proportional staff | High, automation handles increased volume with minimal added cost |

| Implementation timeline | Immediate but inefficient | 3-6 months for initial automation, ongoing optimization |

Barriers SMEs face include credit and skill gaps that make technology adoption challenging. Limited access to capital constrains investment in automation tools. Staff lack technical expertise to implement and maintain sophisticated systems. Fintech partnerships bridge these gaps by providing automation capabilities as managed services rather than requiring in-house development. European fintech accounts for SMEs embed automation features directly into banking platforms, eliminating separate tool costs and integration complexity.

Measure ROI through concrete metrics. Calculate full-time equivalent savings by tracking hours previously spent on manual tasks now automated. Monitor processing time reductions for key workflows like payment approval and reconciliation. Track error rate improvements and their impact on customer satisfaction and operational costs. Operational efficiency in banking studies show well-implemented automation delivers 30-50% cost reductions in targeted processes within the first year.

Pro Tip: Start with high-impact processes like payment reconciliation and routine SEPA transfers to generate quick wins that demonstrate value and build organizational support for expanding automation to more complex workflows.

Scaling automation requires integration capabilities and partnerships. Open banking APIs enable seamless data flow between banking platforms, accounting systems, and business applications. Choose fintech partners with robust API ecosystems and pre-built integrations for common business software. Business account verification processes that leverage automation achieve higher approval rates and faster onboarding, demonstrating how technology partnerships deliver compounding benefits across the customer relationship.

Discover Bankz solutions to streamline your business banking in 2026

Bankz provides automated business banking designed specifically for European SMEs managing cross-border operations. Our multi-currency accounts eliminate conversion costs when you hold funds in the currencies you actually use for international trade. Business debit Visa cards simplify expense management with real-time tracking and automated categorization that syncs directly to your accounting software.

Streamline your business banking operations with Bankz through seamless integration with automation tools and compliance with European regulations. Our platform handles SEPA, SWIFT, and local GBP payments automatically, routing each transaction through the optimal network for speed and cost. Business debit Visa cards provide both physical and virtual options for team spending control. Explore our international business bank account solutions to achieve the operational efficiency and cost savings automation enables.

Frequently asked questions

What is business banking automation?

Business banking automation uses technologies like RPA, AI, and BPM to handle repetitive banking tasks without manual intervention. It automates processes including payments, reconciliation, account opening, and compliance checks, reducing errors and processing time for SMEs.

How much can SMEs save through banking automation?

SMEs typically reduce operational costs by 30-50% in automated processes during the first year. Cross-border transaction fees drop from 3-5% to under 1.5%, while staff time spent on manual reconciliation decreases by 70-80%.

What challenges do SMEs face implementing automation?

Common barriers include limited capital for technology investment, lack of in-house technical expertise, and difficulty integrating legacy systems. Fintech partnerships that provide automation as managed services help SMEs overcome these obstacles without large upfront investments.

How long does it take to implement banking automation?

Initial automation of high-volume processes like payment initiation and reconciliation takes 3-6 months. Full implementation including AI-powered exception handling and predictive analytics typically requires 12-18 months with phased rollout approaches.

Which processes should SMEs automate first?

Start with high-volume, rule-based tasks like payment reconciliation, routine SEPA transfers, and invoice matching. These processes deliver quick wins with measurable time savings and error reduction, building support for automating more complex workflows later.

How does automation handle exceptions and edge cases?

Advanced systems use hybrid AI-human workflows where algorithms resolve standard exceptions automatically and route complex cases to staff with recommended actions. Agentic AI analyzes context and applies cognitive reasoning to ambiguous scenarios, achieving 90% automation rates for exception handling.