Many European business owners worry that remote banking exposes them to fraud and hidden fees, especially when managing multi-currency accounts or cross-border payments. Yet modern remote banking, when properly configured with strong authentication and transparent providers, delivers secure, cost-effective financial management without physical branch visits. This guide explains what remote banking entails, its benefits and risks, and best practices for European businesses navigating international transactions efficiently.

Table of Contents

- Key takeaways

- What is remote banking? Defining the concept and mechanics

- Benefits and challenges of remote banking for European businesses

- Navigating cross-border payments and multi-currency management

- Comparing fintech and incumbent banks in remote banking services

- Explore streamlined remote banking solutions with Bankz

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Remote banking definition | Remote banking lets firms manage accounts and execute transactions through internet channels without visiting a branch. |

| Cost and efficiency gains | It reduces branch visits, speeds operations, and improves cash flow with real time visibility. |

| Fraud risk remains | Despite strong authentication, remote transactions face higher fraud exposure and phishing risks that require vigilance. |

| Transparent pricing matters | Select providers that show fixed fees and real time exchange rates to reduce hidden costs. |

What is remote banking? Defining the concept and mechanics

Remote banking means conducting financial transactions and account management without visiting physical branches. You access your business accounts through digital channels anytime, anywhere with internet connectivity. This shift supports faster decision-making and more efficient financial operations for companies managing European and international cash flows.

Branchless banking encompasses several channels:

- Internet banking via secure web portals for transfers, balance checks, and reporting

- Mobile apps enabling real-time transaction monitoring and approvals

- USSD codes for basic banking in areas with limited connectivity

- Agent-assisted banking through authorized third-party networks

- ATMs and kiosks for cash deposits, withdrawals, and account inquiries

- Dedicated account management software like Bank-Client platforms for corporate treasury functions

Business owners benefit from 24/7 account access, immediate payment execution, and centralized control over multiple currencies and IBANs. Digital banking advantages include reduced administrative overhead, faster reconciliation, and the ability to respond instantly to market opportunities or supplier payment deadlines. Tools like Bank-Client software allow finance teams to initiate bulk payments, configure approval workflows, and generate custom reports without manual branch coordination.

This digital infrastructure proves especially valuable for European SMEs operating across borders. You can monitor euro, pound, and dollar accounts simultaneously, execute SEPA and SWIFT transfers during off-hours, and maintain detailed audit trails for compliance. The technology removes geographic constraints, letting you manage banking from your office, home, or while traveling for business.

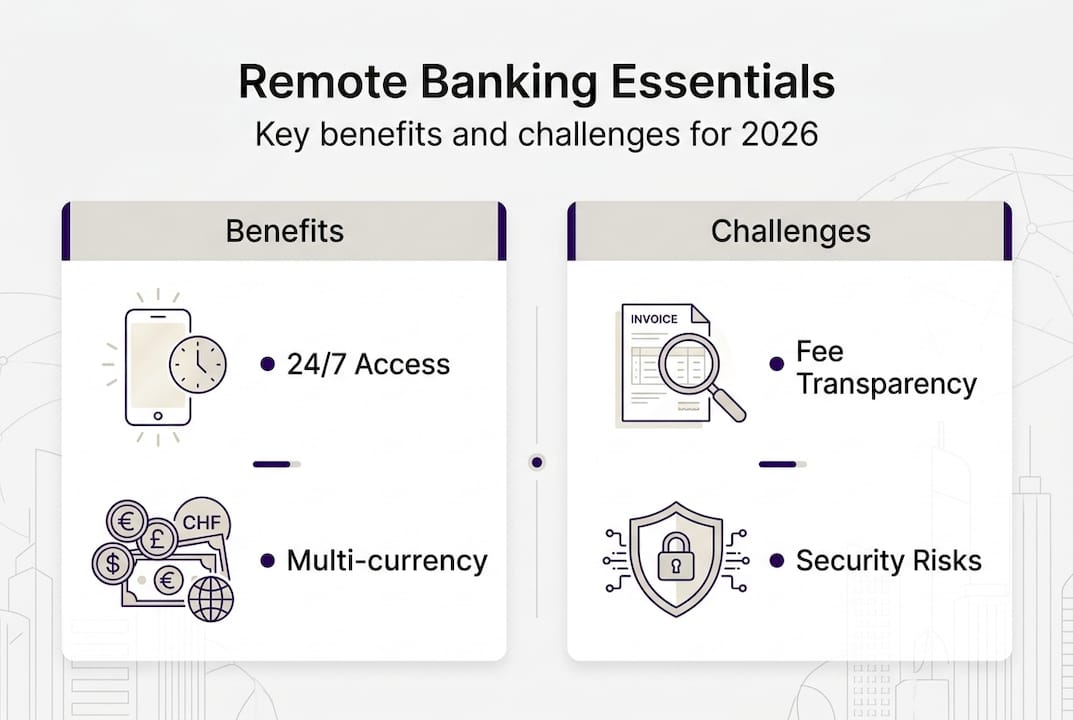

Benefits and challenges of remote banking for European businesses

Remote banking delivers convenience and cost savings by eliminating branch visits and reducing paper-based processes. You save time on travel, queuing, and manual documentation while gaining instant visibility into cash positions across currencies. European branch closures have accelerated business reliance on digital channels, making remote banking essential rather than optional for many SMEs.

Key advantages include:

- Lower operational costs through automated processes and reduced staff time

- Instant access to account balances and transaction histories for better cash flow planning

- Faster payment execution enabling you to capture early payment discounts

- Centralized multi-currency management from a single dashboard

- Scalability to add accounts, users, and services without physical infrastructure

However, remote transactions carry higher fraud risk than in-person banking. In 2024, EU payment fraud totaled EUR4.2 billion, with remote transactions disproportionately targeted. Strong customer authentication (SCA) reduces this exposure significantly, but you must remain vigilant about phishing, credential theft, and social engineering attacks.

"Traditional remote banking offers cost savings and convenience but has security gaps that require robust authentication and monitoring to protect business assets." Remote banking research

Cross-border payment fees in Europe often exceed G20 recommended targets, impacting profitability for businesses making frequent international transfers. Hidden foreign exchange markups and correspondent bank charges can erode margins. The digital divide also creates challenges, as some regions lack reliable connectivity or digital literacy among staff. Varying anti-money laundering (AML) approaches across providers mean you must carefully evaluate compliance rigor, especially if your business operates in sectors facing heightened regulatory scrutiny.

Cutting multi-currency banking costs requires selecting providers with transparent fee structures and competitive exchange rates. Online banking eases financial management for high-risk businesses by offering tailored compliance support and dedicated account managers who understand sector-specific challenges.

Navigating cross-border payments and multi-currency management

Cross-border payments through traditional banks often incur unpredictable costs from foreign exchange spreads, intermediary fees, and delayed settlement. European businesses making regular international transfers need providers offering transparent fixed fees around €5, real-time foreign exchange rates, and cashback incentives that reduce effective transaction costs.

Choose remote banking platforms that provide:

- Fixed transparent pricing with no hidden correspondent bank charges

- Real-time foreign exchange rates updated continuously throughout business hours

- Virtual accounts in local currencies to receive payments without conversion fees

- Local payment rails (SEPA, Faster Payments, domestic ACH) reducing functional distance costs

- Detailed transaction tracking showing exact fees and exchange rates applied

Utilizing virtual accounts lets you hold euros, pounds, and dollars separately, converting only when rates favor your business. This approach minimizes unnecessary foreign exchange transactions and gives you control over timing. Local payment rails reduce functional distance that decreases lending efficiency and increases costs in traditional correspondent banking networks.

Strong Know Your Customer (KYC) processes remain essential as AI-driven fraud attempts rise. Video verification alone proves insufficient against sophisticated deepfake technology and synthetic identity fraud. Your provider should implement multi-layered verification including document authentication, biometric checks, and behavioral analysis to protect your accounts.

| Feature | Traditional Bank | Modern Fintech |

|---|---|---|

| Cross-border fee | €15-€35 variable | €5 fixed |

| FX rate | 2-4% markup | 0.5-1% markup |

| Settlement time | 2-5 business days | Same day or next day |

| Transparency | Limited visibility | Full breakdown |

| Virtual accounts | Rarely offered | Standard feature |

Pro Tip: Regularly review your SCA exemptions and transaction risk profiles. Non-SCA transactions carry higher fraud risk, so limit exemptions to trusted counterparties with established payment patterns. Monitor for unusual transaction sizes, destinations, or timing that deviate from your normal business activity.

Digital business banking drives cross-border success by integrating payment execution, currency management, and compliance monitoring into unified workflows. International business bank account solutions provide the infrastructure European SMEs need to compete globally without the complexity of maintaining relationships with multiple local banks.

Comparing fintech and incumbent banks in remote banking services

Traditional banks offer established security protocols, extensive regulatory compliance, and deposit insurance backing that reassures business owners managing significant balances. Their legacy systems provide stability and proven track records spanning decades. However, innovation cycles move slowly, user interfaces often lag modern standards, and fee structures remain opaque with multiple line items for basic services.

Fintechs deliver user-friendly digital tools, efficient multi-currency account management, and rapid feature deployment responding to market needs. You get intuitive dashboards, instant notifications, and API integrations connecting banking to accounting software. Yet fintech AML rigor varies significantly, with some prioritizing growth over compliance, creating potential regulatory risks for your business.

European SMEs benefit from fintech agility but must evaluate regulatory compliance carefully. Check whether your provider holds appropriate licenses, maintains adequate capital reserves, and subjects itself to regular audits. Verify deposit protection schemes cover your balances and understand what happens to funds if the provider faces financial difficulty.

| Criterion | Traditional Banks | Fintech Providers |

|---|---|---|

| Security infrastructure | Mature, extensively tested | Modern, rapidly evolving |

| Fee transparency | Often opaque, multiple charges | Typically clear, fixed pricing |

| Regulatory compliance | Comprehensive, conservative | Variable, sometimes aggressive |

| Innovation speed | Slow, bureaucratic | Fast, customer-driven |

| User experience | Functional, dated interfaces | Intuitive, mobile-first design |

| Multi-currency support | Limited, expensive | Extensive, competitive rates |

Selecting the right provider depends on several factors:

- Assess your transaction volume and determine whether fixed or percentage-based fees offer better value

- Evaluate your risk exposure and regulatory requirements based on your industry and operating jurisdictions

- Consider your technical capabilities and whether you need API access for accounting integration

- Review customer support availability, especially for time-sensitive payment issues across time zones

- Test the platform with small transactions before migrating significant banking relationships

Pro Tip: Combine fintech services for operational banking with traditional bank relationships for reserve holdings and credit facilities. This hybrid approach balances innovation with stability, giving you competitive transaction costs while maintaining access to established lending and treasury services.

European fintech accounts for SMEs deliver features specifically designed for cross-border commerce, including automated currency conversion triggers and expense categorization. Online banking solutions for startups and SMEs provide scalable infrastructure that grows with your business without requiring system migrations or complex integrations.

Explore streamlined remote banking solutions with Bankz

Managing multi-currency accounts and cross-border payments demands platforms built specifically for European business needs. Bankz offers multi-currency accounts that simplify international transactions through transparent fee structures, real-time exchange rates, and unified dashboards controlling all your currencies and IBANs.

Business debit Visa cards unlock online banking convenience with spending controls, instant transaction notifications, and detailed expense tracking. Physical and virtual cards let you manage team spending, set category limits, and generate reports for accounting reconciliation. The platform integrates SWIFT, SEPA, and local GBP payment options, giving you flexibility to choose the most cost-effective route for each transaction.

Transparent pricing eliminates surprise fees that erode margins on international transfers. You see exact costs before confirming payments, making budgeting predictable and cash flow planning reliable. International business bank account solutions provide the compliance support and dedicated account management European SMEs need to focus on growth rather than banking complexity.

Pro Tip: Use Bankz's integrated monitoring tools to track transaction patterns and identify opportunities to optimize currency conversion timing or consolidate payments for better rates.

FAQ

Is remote banking secure enough for large business transactions?

Yes, when providers implement strong customer authentication (SCA) and robust KYC protocols. SCA reduces fraud rates significantly by requiring multi-factor verification for transactions. Combining encryption, biometric authentication, transaction monitoring, and behavioral analysis makes remote banking safe even for substantial transfers. Choose providers with proven security track records and regular third-party audits. Security with online business banking depends on both provider infrastructure and your internal controls like access management and employee training.

How can I minimize cross-border payment costs using remote banking?

Select platforms with transparent fixed fees and real-time foreign exchange rates rather than traditional banks with opaque pricing. Virtual accounts in local currencies let you receive payments without conversion fees, while local payment rails reduce intermediary costs. Compare providers on total effective cost including FX spreads, not just headline transfer fees. Batch payments when possible and time currency conversions to favorable market rates. Cutting multi-currency banking costs requires evaluating the full cost structure across all your international transactions.

What is the difference between fintech and traditional banks for remote banking?

Fintechs prioritize innovation and user experience with intuitive interfaces, rapid feature deployment, and competitive multi-currency pricing. Traditional banks focus on comprehensive compliance, established security infrastructure, and conservative risk management. Fintechs may compromise on AML rigor to accelerate growth, while incumbents offer reliability but slower innovation cycles. Your choice depends on transaction complexity, regulatory requirements, and whether you value cutting-edge features or proven stability. European fintech accounts for SMEs deliver specialized tools for cross-border commerce that traditional banks rarely match.

What channels does remote banking include for business users?

Remote banking encompasses internet banking via web portals, mobile apps for real-time monitoring, USSD codes for basic functions in low-connectivity areas, agent-assisted banking through authorized networks, ATMs and kiosks for cash transactions, and dedicated software like Bank-Client platforms for corporate treasury. Business users typically rely on web portals and mobile apps for daily operations, with specialized software for bulk payments and complex approval workflows. The channel mix you need depends on your team structure, transaction volume, and geographic footprint.

How do I evaluate a remote banking provider's compliance and security?

Verify the provider holds appropriate banking or e-money licenses from recognized European regulators. Check deposit protection coverage limits and understand the compensation scheme if the provider fails. Review their AML and KYC processes to ensure they meet your industry's regulatory standards. Request information about security certifications, penetration testing frequency, and incident response procedures. Read customer reviews focusing on security incidents and regulatory issues. Test customer support responsiveness with technical and compliance questions before committing significant funds.